(By Faraz Ahmed)

1. The Looming Danger: Anatomy of the Crisis

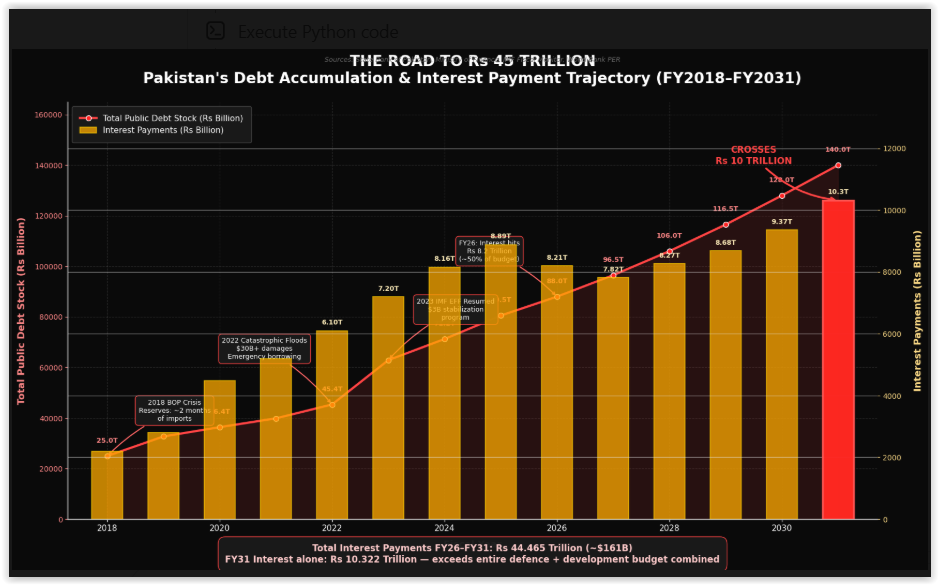

In the early hours of June 2026, as Pakistan’s Ministry of Finance finalized the federal budget, a single line item dwarfed every other national priority combined. Interest payments on public debt—projected at Rs 7.824 trillion for fiscal year 2026–27—will consume nearly half of the entire federal expenditure. But this is not a one-year anomaly. It is the opening act of a fiscal horror story. Over the next five years, Pakistan is projected to spend Rs 44.465 trillion (approximately Rs 45 trillion, or roughly $161 billion) on debt servicing alone. That is not the debt stock. That is merely the interest on what the state has already borrowed. And it is enough to buy a dozen modern metro networks, fund universal primary education for a generation, or build a nationwide renewable energy grid. Instead, it will vanish into the ledger books of creditors—domestic and foreign—leaving the state with fiscal rubble.

The trajectory is relentless. After the Rs 7.824 trillion mark in FY2026–27, interest payments are projected to climb to Rs 8.273 trillion in FY2027–28, Rs 8.681 trillion in FY2028–29, Rs 9.365 trillion in FY2029–30, and finally cross the psychologically devastating Rs 10 trillion threshold in FY2030–31, reaching Rs 10.322 trillion. For the first time in Pakistan’s history, debt interest will exceed Rs 10 trillion in a single year.

To understand what this means in human terms, consider the federal budget’s anatomy. Total outlay for FY26 stood at roughly Rs 17.1 trillion. Interest payments of Rs 8.207 trillion in FY26—later revised to a proposed Rs 7.824 trillion for FY27—consumed approximately 48–50 percent of all federal spending. Defence, at Rs 2.55 trillion, and pensions, at Rs 1.055 trillion, swallowed most of what remained. The Public Sector Development Programme (PSDP)—the engine of infrastructure, schools, and hospitals—shrank to just 4 percent of the budget and 0.6 percent of GDP, down from 19.6 percent of the budget in FY18.

The debt stock behind these payments is staggering. As of February 2026, total federal debt reached Rs 79.9 trillion, including external debt of Rs 23.2 trillion. Gross government debt stood at 70.1 percent of GDP, according to the IMF’s April 2026 Fiscal Monitor. External debt and liabilities surpassed $91.8 billion by June 2025, with federal direct external debt exceeding $82.5 billion.

But here is the crucial nuance that every policymaker must internalize: this is primarily a domestic debt crisis. Over 85 percent of interest payments are on domestic debt owed to local banks, pension funds, and institutional creditors. Even a complete, orderly restructuring of all external debt would barely dent the interest burden. Pakistan is not Greece in 2012, whose crisis was triggered by foreign bondholders. It is more like Japan in the 1990s—except without Japan’s industrial depth, export dominance, or institutional credibility. This is a cash-flow and liquidity crisis masquerading as a solvency debate. The state is not technically broke; it is chronically illiquid, borrowing every month simply to pay last month’s interest, trapped in a treadmill of its own making.

2. The Default Scenario: What Happens If Pakistan Falls

A sovereign default is not a single event. It is a cascade—a domino sequence that begins in finance ministries and ends in food queues. Pakistan must confront this scenario with clear eyes, because the alternative to reform is not “muddling through indefinitely.” It is a multi-dimensional collapse.

Banking & Financial Sector: The Doom Loop

Pakistan’s banking sector is the largest captive buyer of government debt. Domestic banks hold trillions of rupees in government securities, often because regulatory requirements and the absence of robust private-sector credit demand leave them little choice. A domestic debt restructuring—whether a formal “haircut” or a coerced conversion of short-term T-bills into long-term bonds at below-market rates—would instantly wipe out bank capital. The State Bank of Pakistan would face an impossible choice: let the banking system collapse, or print money to recapitalize it, thereby triggering hyperinflation.

This is the “doom loop” between sovereign and banking sectors that devastated Cyprus in 2013 and nearly destroyed Greece. In Pakistan’s case, the loop would be faster and more brutal because the financial sector lacks the depth, derivative hedging, and central-bank credibility that gave Europe time to negotiate. Credit to the private sector would freeze overnight. Businesses would roll over existing loans at punitive rates or fail to access working capital entirely. The formal economy would contract, pushing more activity into the untaxed informal sector, further eroding the revenue base.

External Consequences: Geopolitical Self-Harm

Unlike Argentina or Greece, whose creditors were largely private bondholders who could be negotiated down with minimal diplomatic fallout, Pakistan’s external creditors are almost entirely official: the IMF, the World Bank, the Asian Development Bank, China, Saudi Arabia, the UAE, and the Paris Club. Defaulting on these creditors offers little fiscal relief—concessional loans already carry low interest rates and long maturities—but carries catastrophic geopolitical cost.

Trade credits would dry up. Pakistani exporters would struggle to obtain letters of credit. Asset seizures abroad would become a real risk. Diplomatic relationships built over decades on the premise of “reliable partnership” would fracture. Most dangerously, a default would cut off the concessional financing that Pakistan needs not for luxury, but for survival: balance-of-payments support, flood reconstruction, energy infrastructure, and social safety nets. The state would find itself not just financially paralyzed, but internationally isolated at the precise moment it needs solidarity.

Social & Humanitarian Impact: The Hollow State

With over half the budget already consumed by interest, a default or near-default scenario would force brutal, instantaneous cuts in everything else. Defence spending would face pressure despite existential security challenges. The Benazir Income Support Programme (BISP) and Ehsaas cash transfers—lifelines for millions—would shrink or disappear. Development spending would approach zero.

The social implications are not abstract. Pakistan’s poverty rate, already elevated by inflation that has exceeded 30 percent in recent years, would spike. Unemployment, particularly in the formal sector dependent on bank credit, would surge. The youth bulge—Pakistan’s median age is roughly 22—would face a future without jobs, skills, or hope. Civil unrest, not as a revolutionary movement but as a desperate, fragmented reaction to hunger and inflation, would become a recurring feature of national life.

The “Slow-Burn” Default

There is, however, a more likely scenario than a dramatic, televised default: the “slow-burn” collapse. In this version, Pakistan technically avoids formal default by perpetually rolling over debt, accepting ever-more stringent IMF conditions, and squeezing the economy for just enough revenue to service interest. The result is perpetual stagflation—growth below population increase, inflation chronically above wage growth, and a state that exists but does not function. Schools are built but not staffed. Hospitals have equipment but no medicines. Roads are planned but not paved. The state becomes a debt-paying machine, hollowed out of everything that makes a state worth having.

This is, in many ways, the graver danger. A sudden crisis at least forces decisive action. A slow burn normalizes decay, generation after generation, until the public no longer expects clean water, reliable power, or functioning courts. Pakistan is already halfway there.

3. The India Parallel: “If They Could Do It, So Can We”

In the summer of 1991, India faced an existential economic crisis. Foreign exchange reserves had fallen to $1–2.2 billion—barely enough to cover two weeks of imports. The government airlifted 47 tons of gold to the Bank of England as collateral to secure emergency credit. The rupee was overvalued, the fiscal deficit was ballooning, and industrial growth was sclerotic after decades of “License Raj” controls. In July 1991, India turned to the IMF for a $2.2 billion bailout under a Structural Adjustment Program, complemented by a $500 million World Bank loan.

What happened next is one of the great economic turnaround stories of the late twentieth century. Under Prime Minister Narasimha Rao and Finance Minister Manmohan Singh, India launched a “big bang” reform program that was politically courageous, technically sound, and—crucially—sustained beyond the immediate crisis. The rupee was devalued and moved to a managed float. Industrial licensing was dismantled for all but a handful of strategic sectors. Import tariffs, some as high as 300 percent, were slashed. Foreign direct investment was liberalized, allowing up to 51 percent ownership in key sectors. The stock market was opened to foreign portfolio investors. Tax reform began with the introduction of MODVAT (a precursor to VAT) and eventually culminated in the GST decades later.

The results were not immediate—GDP growth contracted to 0.9 percent in 1991–92 as stabilization bit—but they were durable. By 1992–93, growth rebounded to 4.3 percent. By 1994–95, it reached 6.2 percent. Foreign exchange reserves, which had languished at $2.2 billion in 1990–91, surged to $20.8 billion by 1994–95. Exports grew by nearly 12 percent annually. Foreign investment, projected at $489 million, exploded to $3.2 billion. The central government deficit, which had hit 8.6 percent of GDP in 1990–91, was brought down to 5.7 percent by 1992–93. India’s external debt service ratio improved from crippling levels to 28.3 percent of exports.

The most important lesson was not the specific policy mix but the political economy of reform. Rao and Singh did not have a parliamentary majority. They faced opposition from within their own party, from trade unions, from industrialists who had grown fat on protection, and from state governments wary of federal overreach. Yet they built a reform coalition through a combination of intellectual persuasion, strategic sequencing (reforming trade and industry first, where gains were visible, before tackling the harder task of public-sector restructuring), and sheer persistence. They used the crisis as a lever for change, telling the country: we have no choice but to reform, so let us reform thoroughly.

The Contrast with Pakistan

Pakistan in 2026 is not India in 1991 in every respect. The crisis is deeper, the institutional fabric is more frayed, and the political fragmentation is more severe. But the fundamental challenge—escaping a debt trap through a combination of external discipline, domestic revenue mobilization, and pro-growth structural reforms—is identical.

Consider the divergence in key metrics. India’s tax-to-GDP ratio, around 12 percent at the time of the 1991 crisis, rose steadily over the following decades to approximately 17 percent (federal) and over 25 percent (general government) by the 2010s. Pakistan’s tax-to-GDP ratio has stagnated at roughly 9–10.6 percent for the federal government and around 13 percent for general government—among the lowest in the emerging world.

India’s export-to-GDP ratio grew from roughly 7–8 percent in 1990 to over 20 percent by the mid-2000s, driven by manufacturing, textiles, and later IT services. Pakistan’s export-to-GDP ratio has collapsed from approximately 19 percent in 1990 to roughly 8 percent today—a near-total reversal of the two countries’ trajectories. Where India grew its way out of debt, Pakistan has borrowed its way into stagnation.

The lesson is not that Pakistan must copy India’s exact reforms. It is that a South Asian democracy with deep structural problems, ethnic diversity, institutional weaknesses, and a history of state intervention can escape a debt trap. India proved that the trap is not destiny. It is a choice—a choice made daily through tax policy, trade regulation, and the willingness to confront vested interests.

Pakistan vs. India—Key Economic Indicators at the Time of Crisis

| Indicator | India (1991) | Pakistan (2026) |

|---|---|---|

| Crisis Trigger | Balance-of-payments collapse; reserves covered ~2 weeks of imports | Debt-service spiral; interest consumes ~50% of federal budget |

| Forex Reserves | ~$1.1–2.2 billion | ~$15–20 billion (but heavily indebted) |

| Gross Government Debt | ~75% of GDP | ~70.1% of GDP |

| Tax-to-GDP Ratio | ~12% (rising to 17%+) | ~9.1–10.6% (stagnant for a decade) |

| Export-to-GDP Ratio | ~7–8% (rising rapidly post-reform) | ~8% (fallen from ~19% in 1990) |

| Primary Balance | Deficit; reforms targeted fiscal consolidation | Surplus of 3.2% of GDP in H1 FY26 (IMF program) |

| External Debt Service | ~30% of exports | ~40%+ of exports |

| Key Reform Architects | Narasimha Rao, Manmohan Singh | Politicians guided by Militray |

| Political Context | Weak coalition; built reform consensus | Deep fragmentation; military-civilian divide |

4. The Recovery Roadmap: How to Stay Afloat and Recover

Pakistan does not need a miracle. It needs a plan, executed with the same relentlessness that its creditors apply to debt collection. The roadmap below is structured in three phases: immediate stabilization to prevent collapse; fiscal repair to stop the bleeding; and structural transformation to grow the economy out of the debt trap.

Phase I: Immediate Stabilization (0–18 Months)—Staying Afloat

IMF Discipline as Floor, Not Ceiling. Pakistan’s current Extended Fund Facility (EFF) targets an underlying primary balance of 1.6 percent of GDP in FY2026 and 2 percent in FY2027. The government has, in fact, exceeded these targets in the short term—recording a primary surplus of Rs 4.1 trillion (3.2 percent of GDP) in the first half of FY26, driven partly by expenditure compression.

This is elcome, but it is not enough. The primary surplus must be treated as a floor for survival, not a ceiling for complacency. Every rupee of primary surplus is a rupee not borrowed, and a rupee of debt stock not compounded.

Coordinated Liquidity Support. Pakistan needs synchronized rollovers and concessional financing from China, Saudi Arabia, the UAE, and multilateral lenders. The IMF must act not merely as a lender but as a coordinator—ensuring that bilateral deposits are rolled over, that refinancing is aligned with program reviews, and that no single creditor holds a veto over Pakistan’s stability. The $9 billion in bilateral deposits from friendly countries, representing roughly 9.8 percent of total external debt, must be secured as long-term, stable anchors.

Eliminate Untargeted Subsidies. Fuel and power subsidies, which disproportionately benefit the wealthy and the industrial elite, must be aligned with market prices. The savings—potentially hundreds of billions of rupees—must be redirected to targeted cash transfers through BISP/Ehsaas to protect the vulnerable. The political cost of subsidy removal is high, but the fiscal cost of retaining them is existential.

Emergency Revenue Measures. The government must collect court-ordered “super taxes” and arrears without further delay. Smuggling and under-invoicing at ports—particularly in textiles, electronics, and luxury goods—must be cracked down upon using third-party data and risk-based audits. These are not long-term solutions, but they are essential tourniquets.

Phase II: Fiscal Repair (18 Months–5 Years)—Stopping the Bleeding

Tax Revolution, Not Just Tax Collection. Pakistan’s tax-to-GDP ratio must rise from approximately 9–10.6 percent to at least 15–17 percent, the regional average for comparable economies. This requires four simultaneous actions:

- Broaden the base. Agriculture, which contributes roughly 24 percent of GDP but generates less than 0.1 percent of tax revenue, must be brought into the net through progressive land-based levies and income taxation on large commercial farms. Real estate, which operates as a parallel economy with benami transactions estimated at Rs 4 trillion annually, must face restored capital gains taxation and updated property valuations. Retail and informal trade, which evade documentation through cash transactions, must be integrated via mandatory e-invoicing and point-of-sale reporting.

- Eliminate exemptions. Tax expenditures—special exemptions, deductions, and preferential rates—cost Pakistan between 2 and 3 percent of GDP annually. For FY22 alone, the FBR estimated tax expenditures at over Rs 400 billion in income tax, over Rs 700 billion in sales tax, and over Rs 500 billion in customs. These are not “incentives”; they are fiscal hemorrhages.

- Transform the FBR. The Federal Board of Revenue must be restructured into an autonomous National Revenue Agency, modeled on Bangladesh’s NBR or India’s CBIC, equipped with AI-driven enforcement, integrated databases, and meritocratic staffing. The current fragmentation—14 unconnected IT systems, a broken refund mechanism, and a culture of predatory auditing—must end.

- Harmonize provincial GST. Services, which contribute nearly 58 percent of GDP but are taxed patchily across provinces, require a harmonized GST/VAT regime. Provincial resistance must be overcome through NFC award incentives that reward revenue collection.

Power Sector Surgery. Pakistan’s circular debt in the power sector alone has exceeded Rs 2.9 trillion, with gas sector circular debt adding another Rs 3.4 trillion (2.7 percent of GDP) as of December 2025.

This is not a liquidity problem; it is a structural pricing and governance problem. Tariffs must reflect true costs. Distribution companies (DISCOs) must be privatized or placed under performance contracts with private management. Independent Power Producers (IPPs) must renegotiate capacity payments, with the government willing to accept legal and political pushback to prevent fiscal asphyxiation.

SOE Restructuring/Privatization. Pakistan International Airlines (PIA), Pakistan Steel Mills, and Pakistan Railways are not “strategic assets”; they are fiscal black holes. Loss-making state enterprises must be privatized, restructured, or liquidated. For strategic SOEs where foreign investment is politically sensitive, debt-to-equity swaps with creditors like China should be explored—converting debt into ownership stakes that bring private management discipline.

Export Revival. Pakistan must establish a functional EXIM bank, enhance export refinance facilities, and provide targeted support to manufacturing, IT, and textiles. The goal is not merely to increase export volume but to double exports as a percentage of GDP within a decade. The World Bank’s CGE modeling suggests that comprehensive trade reform—including tariff rationalization and export facilitation—could boost exports by 13 percent, investment by 6.6 percent, and employment by 300,000 jobs in the medium term.

Phase III: Growth & Structural Transformation (5–15 Years)—The India Model

Human Capital Investment. The fiscal dividend from debt stabilization must be invested in education, health, and population management. Pakistan spends less than 2 percent of GDP on education and roughly 0.7 percent on health—fractions of what regional peers allocate. Without skills, Pakistan’s demographic dividend—one of the world’s largest youth cohorts—becomes a demographic time bomb.

Industrial Policy for Export-Led Growth. Pakistan must move decisively from import-substitution to export-led growth. Special Economic Zones (SEZs) must offer genuine infrastructure, regulatory ease, and connectivity—not just tax holidays on paper. The country must position itself as a “China+1” manufacturing alternative, integrating into global value chains where its current participation languishes below 5 percent.

Financial Deepening. Pakistan’s reliance on bank lending and short-term government debt must be reduced through the development of domestic capital markets—corporate bond markets, mortgage-backed securities, and long-term pension funds. A deeper financial sector reduces sovereign-bank co-dependency and provides stable, long-term financing for productive investment.

Debt Management Reform. Borrowing must shift from short-term, high-cost domestic instruments (T-bills, which expose the government to rollover risk and interest-rate volatility) to long-term, concessional external financing for productive infrastructure only. The Debt Policy Coordination Office must be strengthened with independent technical capacity, not just bureaucratic staffing.

5. The Political Economy of Reform: Why It’s Hard

If the roadmap is so clear, why has it not been implemented? The answer is not ignorance. It is power.

Pakistan’s fiscal crisis is not a technical failure; it is a political failure. The root cause is elite capture. Tax-evading lobbies in agriculture and real estate, IPP beneficiaries who extract guaranteed capacity payments regardless of electricity usage, protected industrial sectors that thrive on import tariffs, and real estate speculators who park undocumented wealth in property—these are not marginal actors. They are the backbone of the political funding and patronage networks that sustain governments.

This creates the “reform paradox”: the same crisis that makes reform necessary also makes it politically harder. Austerity breeds unrest. Unrest weakens governments. Weak governments cannot implement reform. The cycle is self-reinforcing.

India escaped this paradox, at least partially, because Narasimha Rao and Manmohan Singh could frame the 1991 crisis as a national emergency requiring national sacrifice. They built a reform coalition that included technocrats, segments of the business community eager for liberalization, and eventually the public, which saw visible gains in consumer choice and economic opportunity.

Pakistan’s challenge is harder. The military, civilian political parties, and judicial institutions have historically operated in separate, often antagonistic spheres. No “national economic compact” has ever held. Yet one is urgently needed. Pakistan’s military establishment, which rightly treats national security as its core mandate, must recognize that fiscal sovereignty is itself a national security issue. A state that cannot pay its soldiers without borrowing from foreign creditors is not strategically autonomous. Civilian parties must accept that partisan advantage cannot come at the cost of institutional destruction. And the judiciary must resist the temptation to block revenue measures—such as agricultural income taxes or property valuation reforms—through populist injunctions.

Transparency as Weapon. Secrecy breeds bad deals. Every international loan agreement, every IPP contract, every debt restructuring term sheet must be tabled in Parliament and published. Parliamentary oversight committees must have the technical capacity—through an independent Budget Office—to scrutinize debt contracts, not just rubber-stamp them. The public must know what its leaders have signed in its name.

6. Conclusion: Radical Pragmatism or Slow Death

Pakistan stands at a 1991-like crossroads. The Rs 45 trillion interest bill is not merely a number. It is a measure of the state’s declining sovereignty. Every rupee paid in interest is a rupee not spent on a classroom, a hospital, a road, or a soldier’s kit. It is a transfer of national wealth to creditors, domestic and foreign, that compounds over time until the state exists to service debt and nothing more.

The choice is binary, even if the transition is gradual. On one path lies radical pragmatism: painful, inclusive, sustained reform that broadens the tax base, privatizes loss-making SOEs, restructures power-sector debt, and invests the fiscal dividend in human capital and export capacity. This path requires political courage, institutional coordination, and a willingness to tell the truth to the public about what has been done and what must be undone.

On the other path lies slow institutional death: perpetual IMF dependence, hollowed-out state capacity, generational poverty, and a slow-burn default in which Pakistan never formally declares bankruptcy but gradually becomes a state that cannot provide water, power, education, or security without foreign permission.

India did not reform in 1991 because it wanted to. It reformed because it had to. The gold airlift to London was a national humiliation that concentrated minds and broke vested interests. Pakistan’s crisis is deeper, but it is not fundamentally different. The numbers are terrifying, the politics are brutal, and the vested interests are entrenched. But the precedent exists, the roadmap is clear, and the alternative is unthinkable.

Pakistan does not need a miracle. It needs what India needed three decades ago: honest accounting, political will, and the courage to let the productive economy breathe. The question is not whether Pakistan can survive. The question is whether its leaders have the courage to do what India did in 1991—before the Rs 45 trillion sword falls, and there is nothing left to save.