(By Khalid Masood)

INTRODUCTION: A NAME FORGED IN EMPIRE AND ECHOED IN CONFLICT

“Whoever controls Hormuz controls the jewel in the ring of the world.”

— Arab geographer’s description, 10th century CE

The name Hormuz carries over a millennium of Persian heritage, maritime ambition, and strategic resonance. Etymologically, it derives from the Middle Persian Hormoz or Ormuz, linguistically tied to Ahura Mazda, the supreme deity of Zoroastrianism representing wisdom and cosmic order. From the 10th to 17th centuries, the Kingdom of Hormuz thrived as a dominant trading empire, controlling commerce across the Persian Gulf and lending its name to the narrow waterway that still bears it today.

The name also echoes in the annals of early Islamic military history. Classical sources, notably the 9th-century historian al-Tabari, record that a Sasanian commander named Hormozd (Hormoz) was killed in single combat by the Rashidun general Khalid ibn al-Walid (RA) at the Battle of Chains (Dhat al-Salasil) in April 633 CE, near modern-day Kuwait. According to these accounts, Hormozd challenged Khalid to a duel; both dismounted, fought hand-to-hand, and Hormozd fell. His death fractured Persian command cohesion and accelerated the Muslim advance into Mesopotamia. While this Hormozd was a provincial governor rather than the direct namesake of the strait, the shared linguistic root underscores a recurring theme: for over fourteen centuries, control of this corridor has been contested by empires, armies, and navies.

Analytical Lens: The persistence of the name “Hormuz” across eras is not incidental. It reflects a deeper truth about strategic geography: certain locations acquire enduring significance because physical constraints—narrow channels, shallow depths, proximity to population centers—cannot be engineered away. The strait’s value is not created by politics; politics is drawn to its value. Understanding Hormuz requires analyzing not just what flows through it, but why its geography makes it irreplaceable, and how that irreplaceability shapes state behavior.

Today, the Strait of Hormuz guards what historians once called “the jewel in the ring of the world.“ It is no longer a jewel of gold or spices, but of hydrocarbons. Through its narrow channels flows roughly one-fifth of global oil consumption and 20% of liquefied natural gas (LNG), making it the single most consequential maritime chokepoint on Earth. Its geography is immutable, its traffic relentless, and its vulnerability a constant variable in global energy security, economic stability, and geopolitical strategy.

“The Strait of Hormuz is not just a chokepoint; it is the jugular vein of the global economy. A sustained closure would trigger an economic shock unlike anything we have seen since the 1970s oil crises.”

— International Energy Agency (IEA)

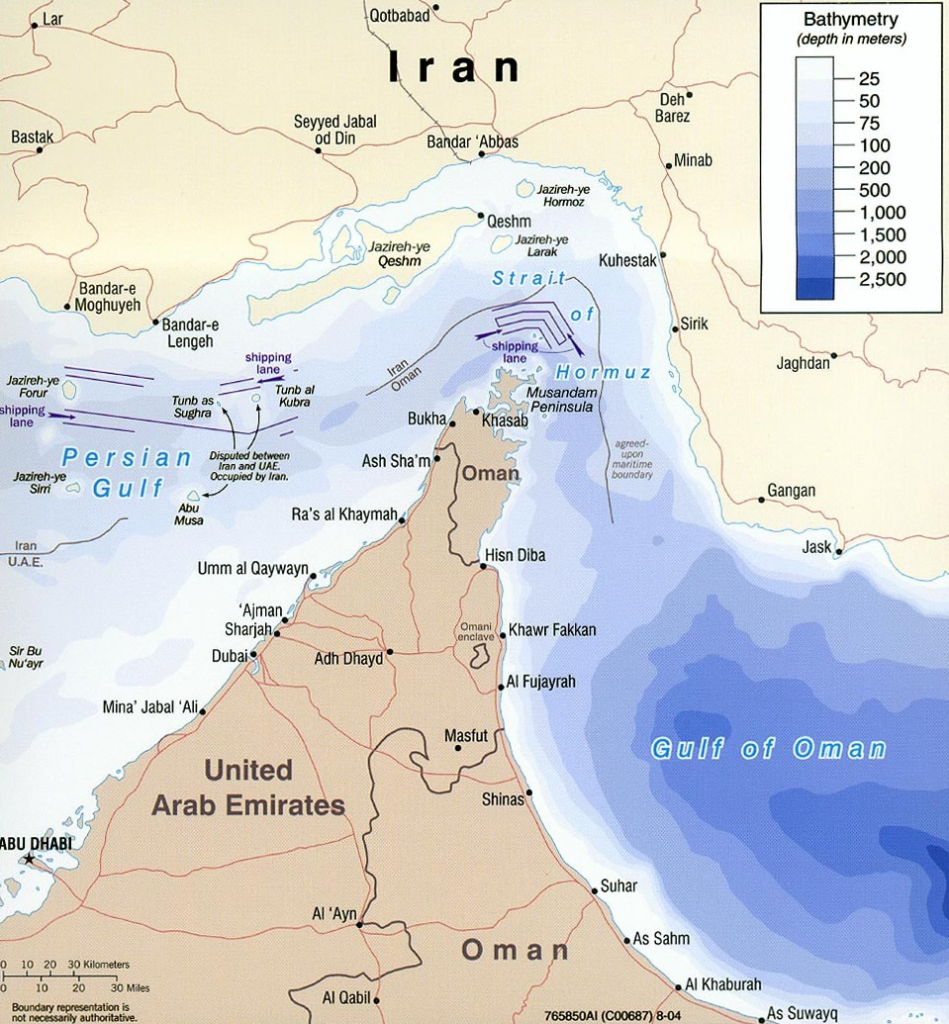

I. GEOGRAPHY & OCEANOGRAPHY: A NATURAL BOTTLENECK

The Strait of Hormuz connects the Persian Gulf to the Gulf of Oman and, ultimately, the Arabian Sea. It lies between Iran to the north and the United Arab Emirates (UAE) to the south.

- Length: ~167 km (104 miles)

- Width: Ranges from ~97 km (60 miles) at its widest to a constraining 33–39 km (21–24 miles) at its narrowest

- Navigable Channels: Traffic is funneled into two 3 km (2 mile), separated by a 3-km buffer zone, to prevent collisions and manage dense commercial flow

- Depth: 60–100 meters (200–330 feet) throughout most of the strait

- Oceanographic Conditions: Sharp salinity and temperature gradients exist between the hypersaline Persian Gulf and the Indian Ocean. Strong tidal currents, seasonal shamal winds, and shallow shoals create challenging navigation conditions, particularly for supertankers and LNG carriers with deep drafts.

Strategic Analysis:

These physical constraints create what military strategists term a “chokepoint advantage” for the defending power. Iran, controlling the northern coastline and high ground, can observe, target, and potentially disrupt traffic with relatively modest investments in coastal defense systems. Conversely, external powers seeking to guarantee freedom of navigation must commit disproportionate resources to mine countermeasures, air defense coverage, and continuous patrol presence.

The narrow, shallow channels also amplify the effectiveness of asymmetric tactics. A handful of naval mines—cheap, concealable, and difficult to detect in busy, sediment-rich waters—can create psychological and operational disruption far exceeding their physical footprint. This asymmetry explains why Iran, despite conventional naval inferiority, can credibly threaten the strait: geography multiplies the impact of limited capabilities.

Comparative Context:

Unlike the Strait of Malacca (wide, deep, flanked by multiple states with shared interests in open shipping) or the Bab el-Mandeb (narrow but with alternative Red Sea routing), Hormuz offers no viable bypass for most Gulf exporters. This uniqueness concentrates risk and elevates its strategic premium.

II. THE ARTERY OF GLOBAL ENERGY: TRAFFIC, VOLUMES & DEPENDENCIES

Under normal operating conditions, the Strait of Hormuz functions as the central artery of global energy trade.

Table 1: Strait of Hormuz Transit Flows & Dependency Metrics (2024–2026 Average)

| Category | Metric | Volume/Percentage | Key Details |

|---|---|---|---|

| Crude Oil & Condensates | Daily Flow | 20.3–20.9 million b/d | ~20% of global consumption |

| Liquefied Natural Gas | Daily Flow | ~20% of global LNG trade | Qatar: 9.3 Bcf/d (83% of strait LNG) |

| Total Vessel Traffic | Annual Transits | 30,000+ vessels | 80–100+ tankers daily |

| Tanker Share | Percentage | 50–60% of all vessels | Oil/gas carriers dominate |

| Saudi Arabia | Export Dependency | ~90% via Hormuz | 7–8 million b/d exports |

| Iraq | Export Dependency | ~95% via Hormuz | 3–3.5 million b/d (southern terminals) |

| UAE | Export Dependency | ~90% via Hormuz | 2.5–3 million b/d + LNG |

| Kuwait | Export Dependency | ~100% via Hormuz | 2–2.5 million b/d |

| Qatar | Export Dependency | 100% via Hormuz | All LNG + condensate exports |

| Iran | Export Dependency | ~90% via Hormuz | 1.5–1.7 million b/d (sanctioned trade) |

| China | Import Dependency | ~50% from Gulf states | 10+ million b/d total imports |

| India | Import Dependency | ~60% from Gulf states | 5+ million b/d total imports |

| Japan | Import Dependency | ~80% oil, 100% Qatari LNG | Critical vulnerability |

| South Korea | Import Dependency | ~70% from Gulf states | Major LNG recipient |

Daily Transit Volumes (2024–2026 Baseline)

“Energy security in the 21st century is not about self-sufficiency; it is about managing interdependence. The Strait of Hormuz is where that interdependence is most concentrated—and most fragile.”

— Dr. Fatih Birol, Executive Director, International Energy Agency

Analytical Insight – The Dependency Paradox:

The strait’s criticality creates a mutual vulnerability: Gulf exporters cannot sell without it, and Asian importers cannot grow without their supplies. This interdependence should, in theory, incentivize cooperation. Yet it also creates leverage: any actor capable of threatening transit gains disproportionate bargaining power. Iran’s toll policy exploits this paradox—imposing modest costs on a system too vital to abandon, betting that the global economy will absorb the fee rather than risk escalation.

Market Structure Analysis:

The concentration of LNG exports through Hormuz (83% from Qatar alone) creates a single-point-of-failure risk distinct from oil. Oil is fungible; a barrel from Saudi Arabia can, in theory, be replaced by one from the U.S. or West Africa. LNG is less flexible: contracts are long-term, infrastructure is destination-specific, and spot markets are thin. A Hormuz disruption would trigger not just price spikes but physical allocation crises, forcing importing nations into zero-sum competition for remaining cargoes.

III. THE $1 PER BARREL TOLL: REVENUE, RISK & MARKET PSYCHOLOGY

In early 2026, Iran introduced a $1 per barrel transit fee for oil tankers passing through the strait, with payments reportedly demanded in cryptocurrency (Bitcoin) or Chinese Yuan. While the headline figure appears modest, its economic and strategic implications are profound.

Revenue Mechanics

- At baseline traffic of ~20.5 million b/d, a strict $1/barrel toll would generate ~$20.5 million per day (~$7.5 billion annually).

- However, open-source tracking and maritime intelligence report Iranian toll collections approaching $139 million per day. This discrepancy reflects a layered system: base tolls, “security processing” fees, insurance premium markups routed through Iranian-linked brokers, and preferential pricing for vessels complying with IRGC inspection protocols.

Impact on Oil Prices

- Direct Cost: Adds ~1–1.5% to crude prices at a $70–80/bbl baseline.

- Indirect/Risk Premium: The toll signals Iranian assertion of control over a global commons. Markets price in uncertainty, adding a $5–15/bbl risk premium. During peak 2026 tensions, Brent crude briefly approached $120/bbl.

- Strategic Paradox: The toll now generates revenue that potentially exceeds Iran’s own pre-crisis oil export earnings (~$139–160M/day from 1.5–1.7M b/d), shifting Tehran’s incentive structure from volume-based exports to control-based rent extraction.

Analytical Framework – Coercive Economic Statecraft:

Iran’s toll policy exemplifies gray-zone coercion: actions that fall below the threshold of armed conflict but achieve strategic objectives through economic pressure. The $1 fee is deliberately calibrated: high enough to generate meaningful revenue and assert sovereignty, low enough to avoid triggering unified military retaliation. It tests the international community’s tolerance for incremental norm erosion.

Behavioral Economics Angle:

Market reactions to the toll reveal a critical insight: perception often outweighs arithmetic. The direct cost impact is minor, but the symbolic message—that Iran can unilaterally impose fees on global commerce—triggers disproportionate risk aversion. Traders price not just the fee, but the precedent it sets. This explains why a $1 toll can move markets more than a $5 production cut from a non-strategic producer.

Policy Dilemma:

Responding to the toll presents a classic collective action problem. Any single importing nation that refuses to pay risks vessel seizure; a unified boycott requires coordination among rivals (e.g., India, China, Japan) with divergent Iran policies. This fragmentation is precisely what Tehran exploits.

IV. CLOSURE SCENARIO: ANATOMY OF A GLOBAL SHOCK

A sustained closure or severe restriction of the strait would trigger the largest energy supply disruption in modern history.

Short-Term (0–30 Days)

- Loss of 20+ million b/d of oil and ~20% of global LNG

- Price Trajectory: $100–150/bbl initially; potential spike to $150–200+ if panic buying and supply hoarding accelerate

- LNG Crisis: Asian spot prices could triple or quadruple. Japan, South Korea, and China face immediate power rationing. Europe faces intensified bidding wars for alternative cargoes.

- Strategic Petroleum Reserves (SPR) IEA member states hold ~4+ billion barrels, sufficient to offset ~30–60 days of losses. After that, physical shortages emerge.

Medium-Term (1–12 Months)

- Demand Destruction: Prices above $120/bbl typically suppress global consumption by 3–5 million b/d through reduced travel, industrial slowdown, and accelerated fuel switching.

- Economic Contraction: Every $10/bbl sustained increase shaves ~0.2–0.3% off global GDP growth. A $50–100/bbl spike risks recession across import-dependent economies and stagflationary pressures worldwide.

- Geopolitical Realignment: Importers accelerate non-Gulf sourcing, naval coalitions expand, and diplomatic pressure intensifies. The risk of military escalation rises sharply.

Risk Assessment Framework:

Not all closure scenarios are equal. Analytical clarity requires distinguishing:

- De facto restriction (delays, inspections, selective access): Manageable with price premiums and diplomatic pressure.

- Partial closure (one lane blocked, traffic reduced 50–70%): Severe economic stress, high escalation risk.

- Full closure (mines, missiles, active combat): Global economic emergency, near-certain military response.

Most likely is a hybrid scenario: Iran maintains “regulatory control” through inspections and tolls, allowing traffic to flow but extracting rents and retaining the option to tighten restrictions. This maximizes leverage while minimizing provocation.

Second-Order Effects Analysis:

Beyond prices, a Hormuz crisis would trigger cascading disruptions:

- Insurance markets: War risk premiums could render some routes commercially unviable.

- Shipping logistics: Rerouting around Africa adds 10–14 days transit time, straining just-in-time supply chains.

- Currency markets: Oil-importing emerging economies face balance-of-payments pressure, potentially triggering capital flight.

- Political stability: Energy-driven inflation could destabilize governments in vulnerable import-dependent states.

V. MILITARY REALITIES & ASYMMETRIC DETERRENCE

Iran’s strategy relies on Anti-Access/Area Denial (A2/AD) rather than conventional naval parity.

Iranian Capabilities

- Coastal Anti-Ship Missiles: Batteries covering the entire strait with ranges up to 300+ km

- Naval Mines: Thousands available; historically proven to disrupt shipping (1980s Tanker War)

- Swarm Tactics: IRGC fast-attack craft (hundreds of vessels) armed with machine guns, rockets, and short-range missiles

- Submarines & UUVs: ~30+ diesel-electric and mini-subs; ideal for shallow-water mine-laying and covert strikes

- Unmanned Systems: Armed drones, USVs, and GPS-spoofing capabilities increasingly deployed for harassment and reconnaissance

Allied Countermeasures

- U.S. Fifth Fleet (Bahrain), UK/French task groups, and GCC navies conduct patrols, mine countermeasure (MCM) operations, and convoy escorts.

- Challenges: Mine clearance is slow and dangerous; swarm defense requires layered air/sea/missile coverage; geographic advantage favors Iran’s northern high ground and coastal concealment.

- Escalation Calculus: Any strike on Iranian territory or IRGC assets risks triggering broader conflict, making containment and deterrence the preferred Western posture.

Strategic Analysis – The Deterrence Equation:

Effective deterrence in the Strait of Hormuz requires balancing three variables:

- Capability: Can allied forces keep lanes open under attack? Technically, yes—but at high cost and risk.

- Credibility: Will allies accept escalation to protect commercial shipping? Historical precedent (Tanker War, 2019 incidents) suggests conditional commitment.

- Communication: Does Iran believe threats of retaliation? Misperception risks abound, especially during crises.

Iran’s asymmetric investments deliberately target the credibility gap: by making retaliation costly and ambiguous, they raise the threshold for external intervention.

Innovation Watch:

Emerging technologies are reshaping the balance:

- AI-enabled target recognition could improve mine detection but also enhance Iranian missile accuracy.

- Swarm drone countermeasures (directed energy, electronic warfare) are advancing but not yet widely deployed.

- Cyber capabilities introduce a new domain: disabling port systems or navigation aids could disrupt traffic without kinetic action.

The side that best integrates conventional, asymmetric, and cyber capabilities will hold the advantage—but integration remains a greater challenge than any single technology.

VI. LEGAL FRAMEWORK & THE QUESTION OF SOVEREIGNTY

Under the 1982 United Nations Convention on the Law of the Sea (UNCLOS), the Strait of Hormuz qualifies as an international strait subject to transit passage (Articles 37–44).

- Transit Passage Rights: Vessels and aircraft may pass continuously and expeditiously without coastal state interference.

- Prohibitions on Coastal States: Cannot suspend passage, impose discriminatory fees, require prior authorization, or hamper navigation.

- Iran’s Position: Signed but never ratified UNCLOS. Claims regulatory authority for “security” and periodically asserts tolling rights.

- Customary International Law: Freedom of navigation is binding even on non-ratifying states. Enforcement, however, depends on naval power and political will, not legal rulings alone.

Analytical Perspective – Law vs. Power:

The Hormuz toll dispute illustrates a foundational tension in international order: legal norms require enforcement mechanisms to be meaningful. UNCLOS provides a clear legal standard, but without naval presence or economic sanctions to uphold it, the law becomes advisory. Iran’s actions test whether the international community will invest the resources to defend a principle (freedom of navigation) when the immediate economic cost of acquiescence appears lower.

Strategic Implication:

If the $1 toll becomes normalized without challenge, it establishes a precedent other chokepoint states (e.g., Indonesia at Malacca, Egypt at Suez) might emulate. The cumulative effect could fragment the global maritime commons into a patchwork of toll regimes, raising transaction costs for world trade. Conversely, a coordinated legal-diplomatic-naval response could reinforce norms and deter copycat behavior.

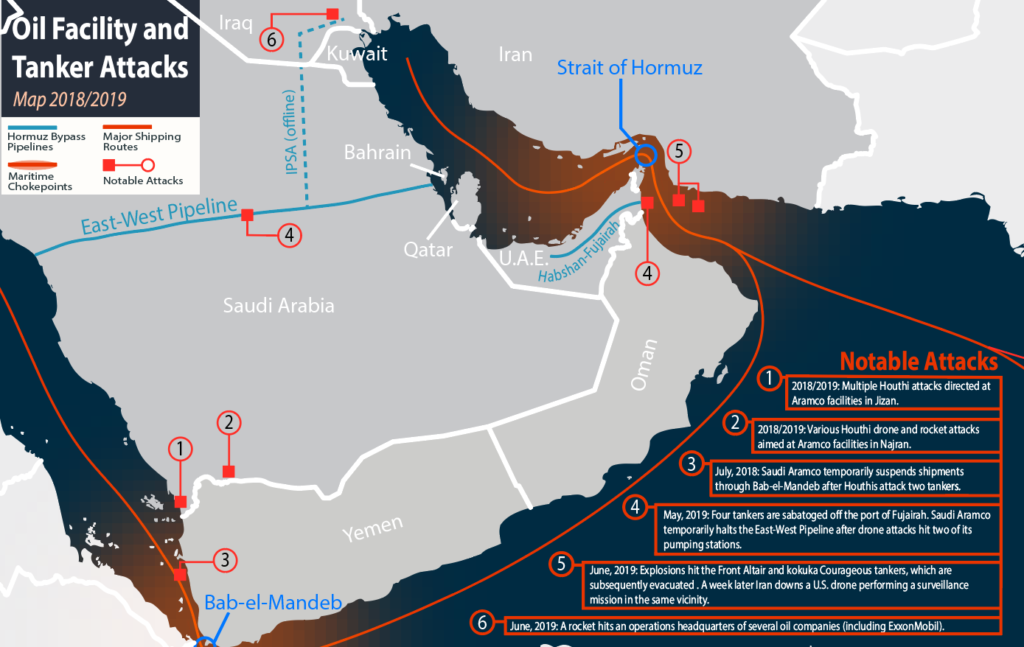

VII. HISTORICAL PRECEDENTS: FROM THE TANKER WAR TO 2026

Table 2: Major Hormuz Strait Crises & Incidents (1980–2026)

| Period/Date | Event | Key Actors | Impact on Traffic | Price Impact | Resolution |

|---|---|---|---|---|---|

| 1984–1988 | Tanker War (Iran-Iraq War) | Iran, Iraq, U.S., Kuwait | 500+ vessels attacked; severe disruption | Volatile; $5–10/bbl premium | U.S. escorts (Op. Earnest Will); UN ceasefire |

| April 1988 | USS Samuel B. Roberts Mining | Iran, U.S. | Temporary lane closures | Spike to ~$22/bbl | U.S. retaliation (Op. Praying Mantis) |

| 2007–2008 | Iranian Speedboat Harassment | IRGC, U.S. Navy | Delays; heightened alert | Contributed to $147/bbl peak | Diplomatic protests; increased patrols |

| May 2019 | Fujairah Sabotage Attacks | Unknown (suspected Iran) | 4 tankers damaged; insurance spikes | +$3–5/bbl risk premium | UAE-Saudi investigation; U.S. deployment |

| June 2019 | Kokuka Courageous Attack | Suspected IRGC | Gulf shipping briefly halted | Brent +5% in days | U.S. blames Iran; IMCM formed |

| July 2019 | British Tanker Seizure | IRGC, UK | Stena Impero detained 4 months | Sustained $5–8/bbl premium | Diplomatic negotiations; eventual release |

| Jan 2020 | Post-Soleimani Tensions | Iran, U.S. | Traffic dropped 30%; insurers withdrew | Brent +7% in week | De-escalation after Iranian missile strike |

| Feb–Mar 2026 | Full-Scale Crisis | Iran, U.S./Israel coalition | 91% traffic drop; 400+ vessels stranded; LNG halted | Brent approached $120/bbl | Ongoing; toll regime instituted |

| April 2026 | $1/Barrel Toll Implementation | Iran, shipping companies | Traffic at 20–30% of normal; IRGC inspections | $5–15/bbl risk premium persists | No resolution; de facto Iranian control |

“History does not repeat itself, but it often rhymes. The Tanker War taught us that harassment is easier than closure, that mines are more effective than missiles, and that international resolve is the ultimate determinant of outcomes.”

— Dr. Anthony Cordesman, Arleigh Burke Chair in Strategy, CSIS

Comparative Historical Analysis:

Three patterns emerge across Hormuz crises:

- Escalation Ladders: Incidents rarely jump directly to war; they proceed through tit-for-tat actions (seizure → sanction → attack → retaliation). Understanding these ladders helps identify off-ramps.

- Adaptive Markets: Shipping companies, insurers, and traders develop workarounds (rerouting, war risk clauses, alternative suppliers), reducing the long-term leverage of disruption—but at increased systemic cost.

- External Power Commitment: U.S. and allied naval presence has been the decisive factor in preventing closure. However, political fatigue and competing global priorities raise questions about the sustainability of this commitment.

Lesson for Policymakers:

History suggests that deterrence works best when it is visible, credible, and coupled with diplomatic channels. Purely military posturing can provoke miscalculation; purely diplomatic engagement can signal weakness. The Tanker War ended not through victory but through a combination of naval protection, UN ceasefire resolution, and war exhaustion. A similar integrated approach may be required today.

VIII. ALTERNATIVE ROUTES & STRATEGIC VULNERABILITIES

No pipeline or corridor can fully replace Hormuz.

- Saudi East-West Pipeline: ~5 million b/d capacity (currently underutilized), exits to Red Sea

- UAE Abu Dhabi Crude Oil Pipeline (ADCOP) ~1.8 million b/d to Fujairah (bypasses strait entirely)

- Iraqi Routes: Limited capacity, constrained by regional instability

- Total Realistic Bypass Capacity: ~5–7 million b/d

- Gap: 13–15 million b/d remains irreplaceably dependent on the strait

Infrastructure Analysis – The Limits of Diversification:

Pipeline alternatives face three structural constraints:

- Geography: Building new pipelines across mountainous or politically unstable terrain is costly and slow.

- Economics: Pipelines require long-term volume commitments to justify investment; uncertain regional stability deters capital.

- Politics: Transit states demand fees, security guarantees, or political concessions, complicating agreements.

Consequently, bypass infrastructure serves as a pressure valve, not a solution. It can mitigate moderate disruptions but cannot absorb a full closure.

Strategic Recommendation:

Rather than pursuing physically vulnerable alternatives, importers should prioritize demand-side resilience: strategic reserves, fuel-switching capabilities, and accelerated energy transition. Reducing dependence on Gulf oil is more sustainable than trying to engineer around its transit constraints.

IX. FUTURE TRAJECTORIES & POLICY IMPERATIVES

Plausible Scenarios (2026–2030)

- Status Quo Toll Regime: Traffic normalizes at 70–85% of baseline; $5–12/bbl risk premium persists; Iran earns $4–7B/year. Manageable but costly.

- Partial Closure/Selective Access: Iran restricts “non-aligned” vessels; prices hit $120–150/bbl; regional recession likely; naval confrontations increase.

- Full Closure & Conflict: Prices surge to $200–300/bbl; global depression risk; major military engagement; long-term supply chain restructuring.

- Diplomatic Resolution: International monitoring mechanism established; tolls removed or minimized under UN/IMO oversight; prices stabilize; freedom of navigation reaffirmed.

Scenario Planning Insight:

The most probable path is not a single scenario but oscillation between them. Iran may tighten restrictions during domestic political pressure or regional tensions, then ease them when economic needs or diplomatic incentives arise. Policy must therefore be adaptive, not static: maintaining deterrence while keeping diplomatic channels open, preparing for disruption without precipitating it.

Strategic Recommendations

- Importers: Coordinate SPR releases, accelerate LNG storage, implement demand management, diversify supply chains, and invest in non-Gulf energy partnerships.

- Exporters: Expand bypass pipelines where feasible, invest in domestic energy transition, and hedge against revenue volatility.

- International Community: Uphold UNCLOS norms, sustain multilateral naval presence, create diplomatic off-ramps, and develop legal-economic frameworks to challenge coercive tolling without triggering escalation.

Analytical Synthesis – The Trilemma of Hormuz Policy:

Policymakers face three competing objectives:

- Keep oil flowing (economic stability)

- Avoid war (humanitarian and strategic imperative)

- Uphold international law (normative commitment)

Optimizing for one often undermines another. For example, accepting tolls keeps oil flowing but erodes legal norms; military enforcement upholds law but risks war. Effective strategy requires sequenced prioritization: short-term focus on flow preservation, medium-term on norm reinforcement through coalition-building, long-term on reducing systemic dependence.

CONCLUSION: THE JUGULAR VEIN OF THE GLOBAL ECONOMY

“In the narrow waters of Hormuz, we find a microcosm of the 21st-century dilemma: how to preserve the benefits of globalization—efficiency, interdependence, prosperity—while building resilience against its vulnerabilities. The answer lies not in retreat from interdependence, but in smarter management of risk.”

— Paraphrased from Dr. Amy Jaffe, Energy Security Expert

The Strait of Hormuz is not merely a geographic feature. It is a structural pillar of the modern energy system, a battleground of asymmetric warfare, and a test of international order. Its 33-kilometer narrowest point carries 20 million barrels of oil daily, powers billions, and dictates economic trajectories across continents.

The $1 per barrel toll may appear numerically small, but it represents a profound shift: the monetization of control over a global commons. Whether it evolves into a stable transit fee, a catalyst for broader conflict, or a bargaining chip in diplomatic negotiations will shape not just energy markets, but the architecture of 21st-century geopolitics.

Final Analytical Reflection:

Chokepoints like Hormuz reveal a fundamental truth about globalization: efficiency creates vulnerability. Just-in-time supply chains, concentrated production, and optimized routing maximize prosperity in stable times but amplify shocks during crises. The strategic challenge is not to eliminate these vulnerabilities—an impossible task—but to build resilience: redundancy in supply, flexibility in demand, and clarity in deterrence.

History shows that chokepoints do not merely channel trade—they channel power. In the Strait of Hormuz, the flow of every barrel is a reminder that energy security, legal norms, and military deterrence remain inextricably linked. How the world navigates this narrow passage will determine whether the global system adapts, fractures, or finds renewed equilibrium.

The name Hormuz, echoing from Zoroastrian temples to Sasanian battlefields to modern tanker decks, reminds us that geography endures while empires rise and fall. The task of statecraft is to ensure that this enduring geography serves commerce, not coercion; connectivity, not conflict.

2 Comments