(By Khalid Masood)

Introduction: When a Maritime Chokepoint Becomes a Harvest Crisis

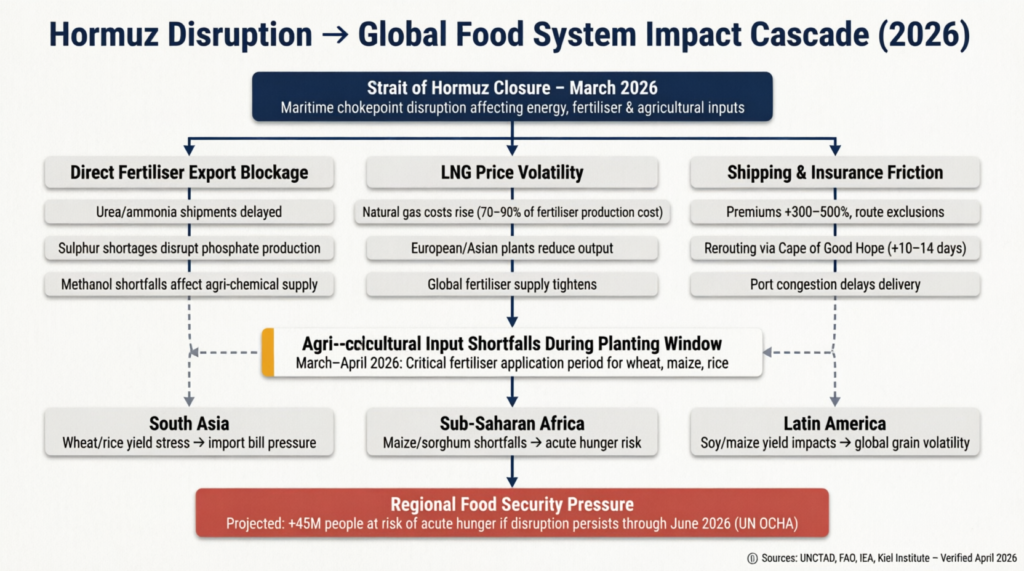

The Strait of Hormuz is widely recognised as a critical energy corridor. Less visible—but equally consequential—is its role in global agricultural supply chains. Approximately46 per cent of seaborne urea, one-third of ammonia and methanol shipments, and significant volumes of sulphur (a key input for phosphate fertilisers) transit the strait annually. When US-Iran war forced the waterway closed to commercial navigation in March 2026, the timing intersected with multiple critical agricultural windows across different hemispheres and cropping systems.

This brief provides a neutral, data-driven assessment of how Hormuz disruptions threaten global harvest cycles, with precise attention to regional crop calendars. It quantifies trade dependencies, analyses region-specific vulnerabilities based on accurate planting and harvesting schedules, and evaluates policy options to decouple humanitarian agricultural trade from broader geopolitical friction. The analysis draws on verified reporting from UNCTAD, the Food and Agriculture Organization (FAO), the International Energy Agency (IEA), and the Kiel Institute for the World Economy.

Verified Trade Flows: Fertiliser, LNG, and Agricultural Inputs via Hormuz

Key Commodities at Risk (2026 Baseline Data)

| Commodity | % of Global Seaborne Trade via Hormuz | Primary Exporters | Top Import-Dependent Regions |

|---|---|---|---|

| Urea | 46% | Iran, Saudi Arabia, Qatar | India (18%), Brazil (10%), China (8%), Pakistan, Bangladesh |

| Ammonia | ~33% | Iran, UAE, Kuwait | East Africa, South Asia, Latin America |

| Methanol | ~33% | Iran, Saudi Arabia | China, India, Southeast Asia |

| Sulphur | ~25% | Saudi Arabia, UAE, Qatar | Morocco (phosphate processing), India, Brazil |

| LNG | ~25% of global supply | Qatar (world’s #1 exporter), Iran | EU, China, Japan, South Korea, Pakistan |

Sources: UNCTAD Review of Maritime Transport 2025; IEA Gas Market Report Q1 2026; FAO Fertiliser Outlook 2026

The LNG-Fertiliser Production Link

Nitrogen-based fertilisers (urea, ammonia) are energy-intensive to produce. Natural gas accounts for 70–90 per cent of manufacturing costs. When Hormuz disruptions spike LNG prices or restrict feedstock access, fertiliser plants in Europe, Asia, and the Americas face a dual pressure: higher input costs and reduced feedstock availability. Preliminary data indicates that European ammonia production capacity utilisation fell by 15–20 per cent in March 2026 alone due to gas price volatility.

“The central issue is not the global average impact, but its distribution. What appears manageable globally becomes a severe food security crisis for the world’s poorest countries.”

— Julian Hinz, Kiel Institute for the World Economy

Accurate Regional Crop Calendars: Timing the Crisis Impact

South Asia (India, Pakistan, Bangladesh)

Two Distinct Agricultural Seasons:

| Season | Crops | Planting Period | Harvest Period | Fertiliser Procurement Window |

|---|---|---|---|---|

| Rabi (Winter) | Wheat, barley, mustard, chickpea | November–December | March–April | September–October |

| Kharif (Monsoon) | Rice, maize, cotton, soybean, sugarcane | April–July | September–November | February–April |

Critical Timing Analysis for March 2026 Disruption:

- Rabi Wheat (Nov–Dec planted, Mar–Apr harvested):

- Fertiliser already applied during planting (Nov–Dec) and top-dressing (Jan–Feb)

- Direct fertiliser impact: Minimal for current crop

- Indirect impact: Harvest logistics, storage, and market access could be affected by broader economic disruption

- Kharif Crops (Apr–Jul planting window):

- March–April is the CRITICAL procurement period for urea, DAP (diammonium phosphate), and NPK fertilisers

- Farmers typically secure inputs 60–90 days before monsoon planting

- Direct impact: SEVERE — fertiliser shortages during March–April directly threaten April–July planting operations

- Expected harvest shortfalls would manifest September–November 2026

Sub-Saharan Africa

Regional Variations by Climate Zone:

| Region | Primary Crops | Main Planting Season | Harvest Period | Fertiliser Procurement |

|---|---|---|---|---|

| West Africa (Nigeria, Ghana, Burkina Faso) | Maize, sorghum, millet, rice | May–June (onset of rains) | September–October | March–May |

| East Africa (Ethiopia, Kenya, Tanzania) | Maize, sorghum, teff, wheat | March–May (long rains); October–November (short rains) | July–September; January–February | January–March; August–September |

| Southern Africa (Zambia, Zimbabwe, Malawi) | Maize, sorghum, tobacco | November–December (onset of rains) | April–June | September–November |

Critical Timing Analysis for March 2026 Disruption:

- East Africa (Long Rains Season):

- March–May planting is underway or imminent

- Direct impact: SEVERE — fertiliser procurement should have occurred January–March; disruption creates immediate shortfall

- Maize and sorghum yields at risk for July–September harvest

- West Africa:

- Preparation phase for May–June planting

- Direct impact: HIGH — March–April is critical procurement window

- Fertiliser distribution systems typically ramp up in March

- Southern Africa:

- Harvest period (April–June) for November–December planted crops

- Direct impact: MODERATE — current crop already established

- Delayed impact: Preparation for next cycle (September–November) could be affected if disruption persists

Latin America (Brazil, Argentina)

| Country | Crop | Season | Planting Period | Harvest Period | Fertiliser Application |

|---|---|---|---|---|---|

| Brazil | Soybean | Main crop | October–November | February–March | September–November |

| Brazil | Maize (Safrinha/2nd crop) | Second crop | January–February | June–July | December–February |

| Brazil | Cotton | Main crop | October–November | March–April | September–November |

| Argentina | Soybean | Main crop | October–December | March–May | September–November |

| Argentina | Maize | Main crop | September–November | March–April | August–October |

Critical Timing Analysis for March 2026 Disruption:

- Brazil Safrinha (Second-Crop) Maize:

- Planted January–February after soybean harvest

- Fertiliser applied during planting (Dec–Feb)

- Direct fertiliser impact: LIMITED for current crop

- Indirect impact: Crop development phase (March–May) may require top-dressing; broader economic disruption affects harvest logistics

- Brazil Cotton & Argentina Soy/Maize:

- Harvest period underway (March–May)

- Direct fertiliser impact: MINIMAL for current harvest

- Delayed impact: Preparation for next planting cycle (September–November 2026) requires fertiliser procurement beginning June–August; prolonged disruption threatens 2026–27 season

- Critical Observation:

- Latin America’s primary fertiliser import window is June–September for the October–November planting season

- If Hormuz disruption persists beyond June 2026, the impact on Latin American agriculture escalates dramatically

Price & Availability Signals

- Urea spot prices rose from ~$350/tonne (January 2026) to over $650/tonne by mid-April 2026

- Diammonium phosphate (DAP) contracts in South Asia saw premium adjustments of +40–60 per cent versus Q4 2025 benchmarks

- Shipping insurance premiums for Persian Gulf agricultural cargo routes increased 300–500 per cent, with some underwriters imposing temporary exclusions

- Indian government reported 35 per cent decline in fertiliser imports during March 2026 compared to March 2025

“If farmers cannot secure fertiliser during their procurement window, the harvest later this year will feel the consequences. The timing mismatch between disruption and planting cycles determines the severity of impact.”

— Frida Youssef, Chief of Transport Section, UNCTAD

Regional Vulnerability Mapping: Who Is Most at Risk?

South Asia (India, Pakistan, Bangladesh)

Agricultural Profile:

- Combined population: ~1.9 billion

- Smallholder dominance: ~85 per cent of farms under 2 hectares

- Fertiliser subsidy programmes critical for affordability

March 2026 Crisis Impact:

| Crop | Current Status (March 2026) | Risk Level | Expected Consequence |

|---|---|---|---|

| Wheat (Rabi) | Harvest underway | LOW (fertiliser already applied) | Minimal yield impact; possible storage/transport disruption |

| Rice (Kharif) | Procurement phase | CRITICAL | Fertiliser shortage threatens April–July transplanting; 15–20% yield reduction possible |

| Maize (Kharif) | Procurement phase | HIGH | Input costs may force area reduction or lower fertiliser application |

| Cotton (Kharif) | Procurement phase | HIGH | Export earnings at risk; smallholder indebtedness likely to increase |

Projected Outcomes:

- Kharif season (2026) fertiliser application could decline 20–30 per cent if disruption persists through April

- Rice production shortfall: 8–12 million tonnes possible (vs. baseline projections)

- Food price inflation: 10–15 per cent projected for Q4 2026

- Rural income loss: $12–18 billion estimated across India, Pakistan, Bangladesh

Sub-Saharan Africa

Agricultural Profile:

- Population: ~1.2 billion

- Fertiliser use lowest globally: ~20 kg/hectare (vs. global average ~140 kg/hectare)

- Import dependence: >70 per cent of fertiliser consumed

March 2026 Crisis Impact by Region:

| Region | Planting Window | Risk Level | Primary Crops at Risk |

|---|---|---|---|

| East Africa | March–May (ongoing) | CRITICAL | Maize, sorghum, teff |

| West Africa | May–June (preparation) | HIGH | Maize, sorghum, millet, rice |

| Southern Africa | November–December (next cycle) | MODERATE (if disruption ends) / HIGH (if persists) | Maize, tobacco |

Projected Outcomes:

- East Africa: 10–15 per cent maize yield reduction possible for July–September 2026 harvest

- West Africa: Fertiliser rationing likely; area planted may decline 5–8 per cent

- Humanitarian impact: 12–18 million additional people at risk of acute food insecurity (World Food Programme estimate)

- Import bill pressure: $2–3 billion additional expenditure for emergency food imports

Latin America (Brazil, Argentina)

Agricultural Profile:

- Major global exporters: Brazil (#1 soy), Argentina (#2 soy, #3 maize)

- Fertiliser import dependence: Brazil ~85 per cent, Argentina ~70 per cent

- Foreign exchange earnings critical for national budgets

March 2026 Crisis Impact:

| Crop | Current Status | Risk Level | Conditional Impact |

|---|---|---|---|

| Brazil Soy | Harvest complete/ongoing | LOW | Minimal direct impact |

| Brazil Safrinha Maize | Development phase | MODERATE | Top-dressing needs; logistics disruption |

| Argentina Soy/Maize | Harvest underway | LOW | Minimal direct impact |

| 2026–27 Season Preparation | 3–6 months away | HIGH (if disruption persists) | June–September procurement window critical |

Projected Outcomes:

- Immediate impact (2026 harvest): Limited to logistical/economic friction

- Delayed impact (2026–27 season): SEVERE if disruption continues beyond June

- Global grain market implications: Brazil/Argentina supply shortfalls would tighten world markets in Q2–Q3 2027

- Export revenue loss: $8–12 billion possible for 2026–27 season if fertiliser access constrained

Systems Diagram: How Hormuz Disruption Cascades to Food Systems

Conflict Resolution Angle: Food Security as a De-Escalation Lever

Humanitarian Corridors for Agri-Inputs

Proposal: Establish UN-monitored “green lanes” for fertiliser, seed, and food shipments, operationally separate from military logistics, with priority routing based on regional planting calendars.

Timing-Sensitive Implementation:

- Immediate priority (March–April 2026): South Asian Kharif fertiliser shipments, East African planting inputs

- Secondary priority (May–June 2026): West African pre-planting fertiliser distribution

- Tertiary priority (June–September 2026): Latin American 2026–27 season preparation

Precedent: The Black Sea Grain Initiative (2022–2023) demonstrated that negotiated agricultural corridors can function amid active conflict, provided verification mechanisms are robust and politically insulated.

Implementation Considerations:

- Third-party inspection teams (e.g., UN/ICAO-affiliated)

- Pre-cleared vessel lists updated quarterly based on planting calendars

- Real-time cargo tracking via satellite AIS

- Regional distribution hubs to minimise last-mile delays

Strategic Reserve Coordination

Regional Buffer Mechanisms:

- South Asia: Activate SAARC Food Security Reserve; coordinate fertiliser sharing between India, Pakistan, Bangladesh based on crop calendar priorities.

- Sub-Saharan Africa: Leverage AU’s African Fertiliser and Agribusiness Partnership (AFAP) emergency protocols

- Latin America: Utilise MERCOSUR agricultural cooperation frameworks for fertiliser redistribution

Kiel Institute Recommendation: “Strategic fertiliser reserves in import-dependent countries, coupled with transparent release protocols tied to planting calendars, could mitigate short-term shocks while longer-term supply diversification proceeds.”

No-Code Workflow Tip: Use publicly available FAO GIEWS (Global Information and Early Warning System) data to build simple dashboards tracking regional buffer levels against planting window timelines.

Decoupling Humanitarian Trade from Sanctions Enforcement

Policy Clarity: Advocate for explicit exemptions for agricultural inputs under existing sanctions regimes, with clear definitions of “humanitarian fertiliser” based on crop calendar urgency.

UNCTAD Guidance: “There is a shared global interest in keeping trade routes open for essential goods, because disruptions of this scale affect all economies—especially the most vulnerable. Timing-sensitive agricultural inputs require expedited processing.”

Verification Focus:

- Transparent cargo manifests with crop calendar justification

- End-use monitoring via satellite imagery and local agricultural extension services

- Digital tracking from port to farm gate

- Independent audit mechanisms to prevent diversion

Conclusion: Data, Timing, and the Case for Preventive Diplomacy

The 2026 Strait of Hormuz closure illustrates how maritime chokepoints can transmit geopolitical friction into global food systems with remarkable speed—and with highly variable impacts depending on regional crop calendars. The convergence of disrupted fertiliser flows, LNG price volatility, and the inflexible timing of agricultural cycles creates multiple narrow windows for preventive action.

Critical Timing Summary:

- South Asia: March–April 2026 is the decisive procurement window for Kharif season (April–July planting); delays now will manifest as harvest shortfalls in September–November 2026

- Sub-Saharan Africa: East Africa faces immediate crisis (March–May planting); West Africa has a 60–90 day buffer; Southern Africa’s risk escalates if disruption extends beyond June

- Latin America: Current harvest largely secure; however, June–September 2026 procurement for the 2026–27 season represents a critical vulnerability

Neutral, evidence-based analysis suggests that targeted diplomatic measures—humanitarian corridors prioritised by planting calendar urgency, strategic reserve coordination, and sanctions decoupling for time-sensitive agricultural inputs—could mitigate the most severe food security outcomes without compromising broader security objectives. Critically, these measures require verification mechanisms insulated from political narratives, alongside phased implementation tied to transparent compliance metrics and regional agricultural calendars.

As planting windows open and close across different hemispheres, policymakers, humanitarian agencies, and agricultural stakeholders must prioritise data-driven, calendar-aware risk assessment over escalation narratives. Ongoing monitoring of fertiliser price signals, shipping logistics, regional planting progress, and crop development stages will be essential to anticipate and respond to emerging food system stresses.

The next 90 days (April–June 2026) will determine whether this crisis remains a manageable disruption or escalates into a multi-regional food security emergency affecting the 2026–27 agricultural cycle.