(By Khalid Masood)

Introduction

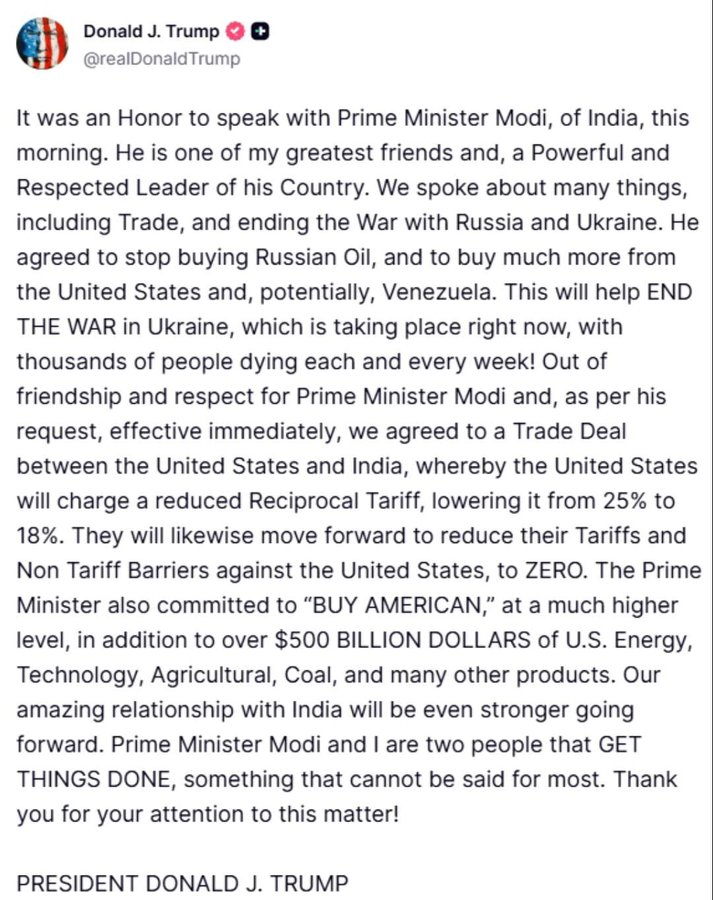

On 2 February 2026, in a development that unfolded with remarkable speed, US President Donald Trump announced via Truth Social that the United States and India had reached a bilateral trade agreement following a phone call with Indian Prime Minister Narendra Modi. The centrepiece of the announcement was an immediate reduction in US tariffs on Indian goods from an effective 50% to 18%. This adjustment sent ripples across global markets, with India’s benchmark Nifty 50 index surging approximately 5% at the open the following day.

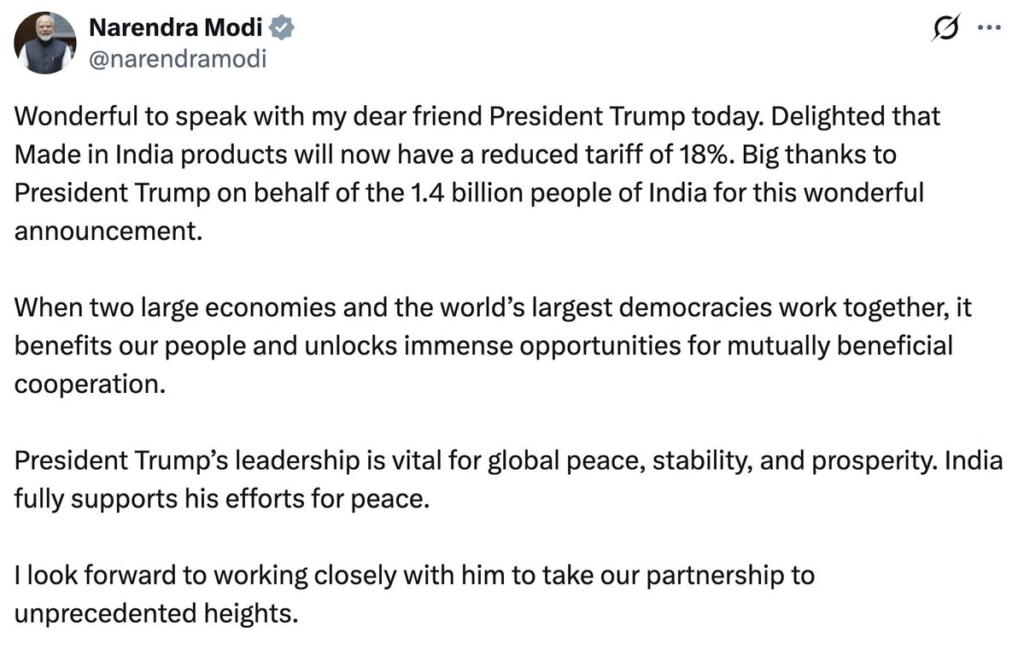

The deal’s timing and framing were striking. Trump attributed the swift resolution to “friendship and respect” for Modi, noting it came “as per his request.” Modi, in turn, expressed delight that “Made in India products will now have a reduced tariff of 18%,” thanking Trump on behalf of India’s 1.4 billion people and pledging support for US efforts toward global peace, stability, and prosperity. The agreement appeared to resolve months of trade friction rooted in Trump’s broader “reciprocal” tariff regime and specific punitive measures tied to energy geopolitics.

For South Asia, the implications extend far beyond bilateral US-India ties. Pakistan, facing a 19% US reciprocal tariff on most exports (established in August 2025 after negotiations reduced an initial 29% proposal), now contends with a slight but tangible competitive disadvantage against India in the American market. This US dynamic compounds an even more pressing challenge: India’s landmark Free Trade Agreement (FTA) with the European Union, concluded on 27 January 2026 and widely termed the “mother of all deals.” That pact grants India near-comprehensive duty-free access to the EU, threatening to erode Pakistan’s preferential edge under the EU’s Generalized Scheme of Preferences Plus (GSP+).

In a world increasingly characterised by trade fragmentation, personalised diplomacy, and geopolitical leverage, these developments highlight how swiftly alliances and concessions can alter export competitiveness. This comprehensive analysis explores the mechanics of the India-US breakthrough, its historical and geopolitical context, sector-specific impacts on Pakistan in the US market, the added pressure from the India-EU FTA, broader regional implications, comparative perspectives, and strategic considerations for Islamabad.

India-US Deal Mechanics, Concessions, and Immediate Effects

The agreement’s core adjustment addressed a two-layered tariff structure imposed during 2025. The base “reciprocal” tariff stood at 25%, part of Trump’s policy targeting countries with perceived trade imbalances or high barriers against US goods. An additional 25% punitive duty was layered on top specifically for nations continuing to purchase discounted Russian crude oil—viewed by Washington as indirectly supporting Russia’s war in Ukraine. India’s effective 50% rate was thus unique among major trading partners.

Trump’s announcement confirmed the reduction to 18%: the punitive 25% levy was removed entirely, and the base reciprocal rate was lowered from 25% to 18%. A White House official clarified that this rescinded the Russia-related penalty in full. In exchange, India committed to halting or significantly reducing purchases of Russian oil, redirecting sourcing toward US energy supplies and potentially Venezuelan crude as an alternative. Trump claimed India would “buy much more” from the US, citing over $500 billion in purchases over time across energy, agriculture, technology, coal, and other products. India also pledged to reduce its own tariffs and non-tariff barriers on US goods toward zero, with a focus on agriculture—a persistent US demand.

The deal’s interim character was evident: described as the first tranche, it lays groundwork for a more comprehensive Bilateral Trade Agreement (BTA). Full implementation details, including exact timelines for oil shifts, sector-specific commitments, and barrier reductions, remain limited in public disclosures. Modi emphasised benefits for “Made in India” initiatives, while Trump framed the pact as mutually reinforcing for the world’s two largest democracies.

Market reactions in India were immediate and positive. The Nifty 50’s 5% jump reflected optimism in labour-intensive and export-oriented sectors. Textiles, apparel, gems and jewellery, chemicals, fisheries, and manufacturing stand to gain most from restored price competitiveness in the US. For instance, Indian apparel exporters previously constrained by high duties could see revived volumes in price-sensitive categories, potentially boosting employment in states like Tamil Nadu and Gujarat. One might reasonably ask: in a global environment of supply-chain diversification away from China, could this deal accelerate India’s emergence as a preferred alternative for US buyers?

Historical Context of the 2025 Tariffs and Geopolitical Drivers

Trump’s second-term trade policy revived and expanded “reciprocal” tariffs, invoking national emergency powers to address persistent US trade deficits. From April 2025, a baseline 10% tariff applied broadly, with country-specific rates phased in by August following negotiations. Punitive “secondary” measures targeted buyers of Russian-origin goods, including oil, to economically pressure Moscow amid the ongoing Ukraine conflict.

India’s 50% effective rate stemmed directly from this framework: the 25% reciprocal baseline plus the 25% Russia-related penalty. Tensions peaked when Trump publicly labelled India the “tariff king” earlier in his term, highlighting asymmetries in market access. Negotiations stalled amid broader frictions, including differing views on energy sourcing and strategic autonomy.

The breakthrough reflects classic transactional diplomacy. Tariffs functioned as leverage (sticks), while concessions on energy diversification and market opening served as carrots. Trump’s style—emphasising personal rapport—proved pivotal; frequent references to “friendship” and Modi’s “request” underscore how leadership ties expedited resolution. For India, the adjustment balances strategic autonomy (longstanding Russia ties) with pragmatic economic needs: protecting exports amid elevated global oil prices and supply-chain uncertainties.

Sector-by-Sector Impact on Pakistan in the US Market

Pakistan’s US exports, valued at roughly $5–6 billion annually before tariff escalations, remain dominated by textiles, apparel, and home goods (approximately 70–80% of the total). Other notable categories include basmati and non-basmati rice, leather goods, surgical instruments, and sports goods from specialised clusters like Sialkot.

Pakistan operates under a 19% reciprocal tariff, finalised in August 2025 after Islamabad secured concessions through commitments on oil reserves, critical minerals, and strategic cooperation. No additional punitive layer applies, unlike India’s former structure. However, India’s reduction to 18% introduces a 1% differential that lowers Indian landed costs and enhances price competitiveness.

Sector-specific vulnerabilities include:

- Textiles and apparel: Pakistan’s flagship category faces the greatest risk. Experts suggest a potential 5–10% market share diversion to Indian suppliers, translating to annual losses of $300–600 million. Lower duties could enable Indian exporters to undercut Pakistani prices in mid-range segments like knitwear, bed linens, and towels.

- Rice: Indian basmati and non-basmati varieties gain a restored edge, intensifying direct competition in premium US markets.

- Niche clusters (e.g., Sialkot surgical instruments and sports goods): These labour-intensive, price-sensitive products are particularly exposed, as even small cost advantages compound over large volumes.

No signals of imminent further relief for Pakistan have emerged, despite warmer bilateral engagements. Without comparable leverage—such as major energy shifts or large-scale US purchases—Pakistan’s exporters face renewed margin pressure, potentially straining foreign exchange reserves, factory utilisation, and jobs in Punjab and Sindh provinces.

India’s EU FTA Details and How It Squeezes Pakistani Exports in Europe

Concluded on 27 January 2026 after nearly two decades of negotiations, the India-EU FTA—hailed as the “mother of all deals”—delivers unprecedented access. It eliminates or sharply reduces tariffs on approximately 93–99% of Indian exports by value. Immediate zero duties apply to 70.4% of tariff lines, covering 90.7% of exports in labour-intensive sectors including textiles, leather, footwear, tea, coffee, spices, sports goods, toys, gems and jewellery, and select marine products. Phased reductions cover remaining lines, with full effects anticipated by 2027–2028 following ratification.

The EU constitutes Pakistan’s largest export destination, accounting for about 27% of total exports (roughly $8–9 billion annually), with textiles and apparel comprising around 75%. Pakistan benefits from GSP+ preferences, granting duty-free/quota-free access on 66–85% of lines until December 2027, though renewal faces uncertainty due to EU scrutiny over labour rights, human rights, and competitive pressures.

The squeeze is acute:

- Textiles and apparel: Pakistan’s current 5–9% preference margin evaporates as India gains zero/low tariffs. Industry estimates indicate a potential 15% share loss, equating to approximately $1.5 billion in annual erosion—devastating for an employment-heavy sector.

- Leather, footwear, and labour-intensive goods: Similar dynamics threaten clusters in Sialkot and Karachi, where scale and diversification favour India.

- Broader risks: If GSP+ lapses post-2027—amid concerns over governance or FTA-driven competition—Pakistan would confront full Most Favoured Nation tariffs while India enjoys sustained preferences.

Exporters and analysts in Pakistan have voiced alarm, warning that the combined US and EU pressures could undermine billions in trade value unless addressed urgently.

Geopolitical Implications, Comparisons to Other US Deals, and Strategic Outlook for Pakistan

Geopolitically, the US wields tariffs as tools for concessions, with Trump’s approach prioritising personal diplomacy and energy security. India’s pivot from Russian oil aligns with Western isolation efforts while safeguarding economic interests. Pakistan’s multipolar posture—balancing China partnerships, Russia ties, and US engagement—limits scope for equivalent breakthroughs.

Comparatively, Pakistan’s 19% US rate aligns with peers like Vietnam and Thailand (around 19–20%) and Bangladesh (20%), but trails India’s new 18% and South Korea’s negotiated 15%. India’s aggressive FTA strategy (EU and others) positions it as a China counterweight and supply-chain diversifier in fragmented global trade.

Pakistan’s outlook requires proactive steps: accelerating FTA negotiations (EU, UK, GCC), diversifying markets (China, Middle East), and pursuing domestic reforms to lower energy costs, enhance productivity, and improve competitiveness. Combined export losses across US and EU could reach $2–4 billion annually if unmitigated, underscoring the need for agility.

Conclusion – Broader Lessons on Trade Diplomacy in a Fragmented World

The India–US trade breakthrough announced in early February 2026 demonstrates how transactional diplomacy, strong personal rapport between leaders, and carefully calibrated concessions can swiftly transform entrenched trade tensions into opportunities.

For India, the deal—heralded as a major win by both sides—involves significant concessions in exchange for relief from punishing U.S. tariffs (slashed from as high as 50% to 18% on Indian exports). Key elements include a phased reduction in purchases of discounted Russian oil (with a shift toward U.S. and potentially Venezuelan supplies), commitments to substantially increase imports of American goods (with figures cited around $500 billion over time across sectors like energy, technology, agriculture, defense, aircraft, and more), and lowering Indian tariffs on many U.S. products toward zero in key areas. These terms are undoubtedly demanding and have sparked debate about short-term costs—especially higher energy import bills and adjustments in strategic sourcing.

Yet, the long-term calculus appears more favorable for India: restored export competitiveness in the massive U.S. market, stronger positioning in global supply chains (particularly as an alternative to China), boosted manufacturing and sectors like IT/pharma/textiles, and enhanced geopolitical alignment amid shifting alliances. Combined with the recently concluded India–EU Free Trade Agreement (finalized just days earlier in late January 2026, granting near-zero duty access for most Indian exports to Europe), these pacts position India as a central player in a multipolar trade landscape.

For Pakistan—and other smaller or mid-tier economies—the picture is sobering. The dual pressure from U.S. tariff structures (favoring partners like India) and the India–EU FTA (which could divert trade flows and heighten competition in key export sectors) highlights the vulnerabilities of nations caught in geopolitical fragmentation. Without comparable leverage or deals, risks of marginalization grow, including reduced market access, slower export growth, and greater dependence on volatile commodity channels.

Resilience, however, remains possible through deliberate strategies: accelerating export diversification (beyond textiles to higher-value sectors), pursuing domestic reforms for competitiveness (e.g., energy, logistics, and regulatory ease), deepening ties with alternative markets (Middle East, ASEAN, Africa), and proactive diplomatic outreach to major powers. Forward risks include further isolation if global blocs harden, but opportunities lie in nimble pivots—perhaps leveraging regional frameworks like ECO or seeking balanced engagements with both East and West.

What are your thoughts on Pakistan’s path forward in this rapidly evolving trade environment? Do you see viable strategies in specific sectors (e.g., IT, agriculture, renewables), geopolitical balancing acts, or urgent policy priorities? Share your perspectives in the comments—let’s discuss how South Asia can navigate these shifting currents effectively.