(By Khalid Masood)

I. The Chokepoint Gambit

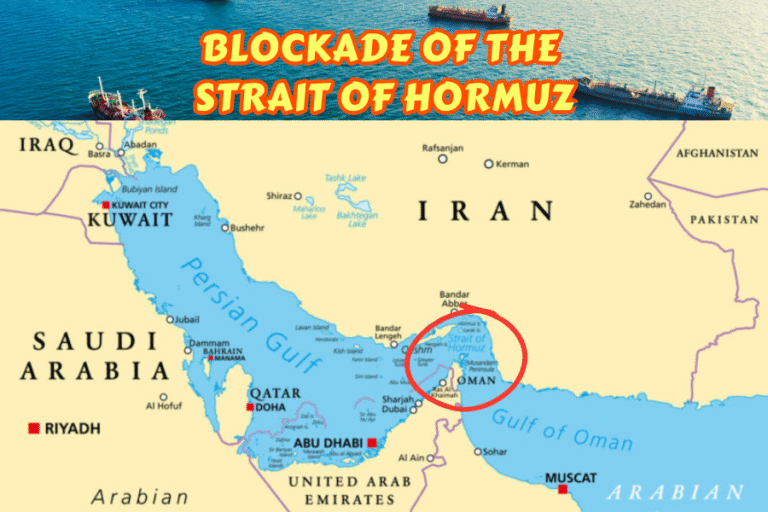

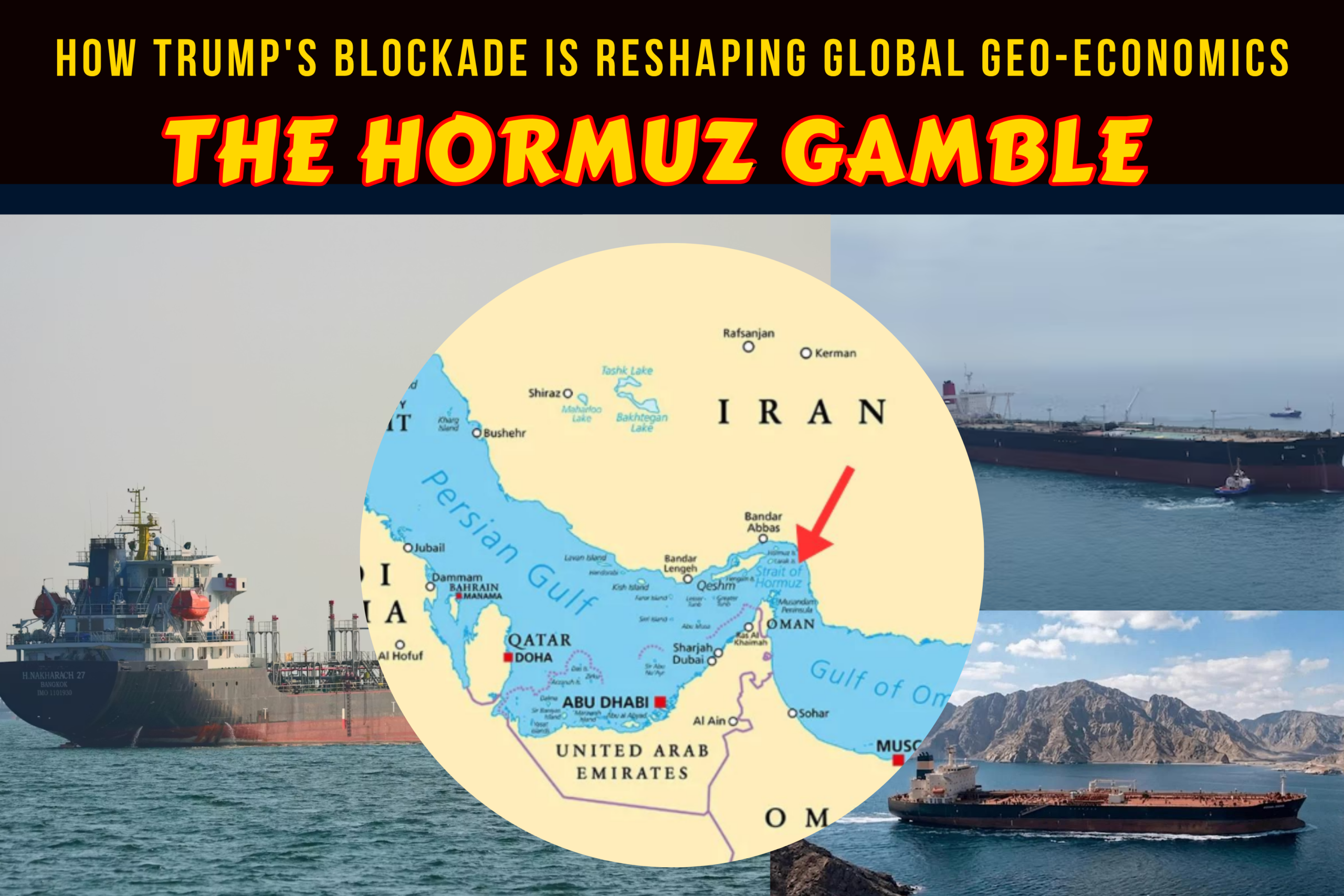

At 3:47 a.m. on 4 March 2026, the master of the VLCC Frontline Voyager radioed a panicked message to the United Kingdom Maritime Trade Operations centre in Dubai: “Strait closed. Mines sighted. All traffic halted.” Within seventy-two hours, 150 tankers lay anchored in the Gulf of Oman, their hulls carrying 20 million barrels of crude that would not reach Rotterdam, Mumbai, or Yokohama for weeks—if at all. The Strait of Hormuz, that slender 21-mile maritime throat through which one-fifth of the world’s oil and one-fifth of its liquefied natural gas must pass, had become a weapon of war.

Iran’s closure of the strait was not merely tactical retaliation for the American-Israeli assassination of Supreme Leader Ali Khamenei on 28 February—an operation the Pentagon codenamed “Epic Fury.” It was, in the parlance of strategic theorists, horizontal escalation: the deliberate extension of conflict into economic and political realms to raise costs for the adversary beyond what military endurance alone could sustain. As one Iranian Revolutionary Guard Corps commander reportedly told state television, “If they strike our cities, we shall strike their economies.”

Yet if Tehran gambled that choking global energy flows would force Washington to relent, President Donald Trump raised the stakes still further. On 13 April, the United States Navy imposed a counter-blockade on Iranian ports, preventing inbound vessels from reaching terminals at Bandar Abbas, Kharg Island, and Asaluyeh. The result is a “dual blockade” unprecedented in modern maritime history: Iran holds outbound Gulf exports hostage, whilst the United States holds inbound Iranian trade captive. Both sides have transformed the world’s most critical energy artery into a bargaining chip—and the global economy is paying the price.

This article argues that Trump’s Hormuz gamble is not merely a military tactic but a geo-economic watershed. It is accelerating the fracture of the post-Cold War order, exposing the lethal vulnerability of maritime chokepoints, and catalysing a structural realignment of global energy architecture that will outlast the war itself. The blockade is a tactic; the transformation it has unleashed is strategic and permanent.

II. The Dual Blockade: Anatomy of a Global Energy Shock

The Iranian Closure

Iran’s mining of the strait began within hours of Khamenei’s death. By 10 March, tanker traffic had dropped 70 per cent; by mid-March, it had fallen to near-zero. The International Maritime Organization reported that 20,000 mariners aboard 2,000 vessels were stranded in the Persian Gulf, their crews rationing provisions whilst insurers withdrew coverage and charterers cancelled contracts.

The legal dimension was equally stark. Under Article 44 of the United Nations Convention on the Law of the Sea (UNCLOS), states bordering straits used for international navigation are explicitly prohibited from hampering transit passage. Iran’s closure was not merely an act of war but a breach of international maritime law that stripped the strait of its legal protections. As Professor James Kraska of the U.S. Naval War College observed, “Iran has turned a legal commons into a contested battlespace, and in doing so, invited the very countermeasures that now trap its own commerce.“

The American Counter-Blockade

Trump’s response combined naval force with theatrical brinkmanship. Between 22 March and 7 April, the President issued a series of ultimata via Truth Social, threatening Iranian power stations, bridges, and desalination plants with destruction. On 6 April, he posted: “A whole civilisation will die tonight.” The following day, U.S. warships began interdicting vessels bound for Iranian ports, creating a symmetrical blockade that paralysed both sides of the Gulf’s maritime economy.

The dual blockade dynamic is the critical innovation of this crisis. Unlike previous Hormuz confrontations—1984’s Tanker War, 2019’s sabotage campaign, 2021’s seizure incidents—both belligerents now hold the strait hostage. Iran blocks the exit; the United States blocks the entrance. The result is not a siege but a strangulation of the entire Gulf maritime system.

Market Catastrophe

The economic impact was immediate and devastating. Brent crude surged past $120 per barrel in early March, peaking at $126 by mid-month—the largest monthly oil price increase in history (As of now the price is $ 113.94). The International Energy Agency reported that Gulf oil production dropped 6.7 million barrels per day by 10 March, rising to over 10 million bpd by 12 March. Russell Hardy, chief executive of Vitol, the world’s largest independent oil trader, warned that “one billion barrels of production will be lost” before the crisis resolves.

The LNG market fared worse. QatarEnergy, the state-owned giant operating Ras Laffan—the world’s largest liquefaction facility, accounting for 20 per cent of global LNG exports—declared force majeure on all shipments. Asian spot prices doubled to $25.40 per million British thermal units, triggering emergency rationing in Japan and South Korea and forcing Pakistan and Bangladesh to halt industrial gas supply entirely.

| Key Market Indicators: Hormuz Crisis (March–April 2026) | |

|---|---|

| Metric | Figure |

| Brent crude peak | $126/barrel (on 2 May : $ 113.94) |

| Gulf oil production loss | 10+ million bpd |

| LNG spot price (Asia) | $25.40/MMBtu |

| Estimated production loss (Vitol) | 1 billion barrels |

| Ships stranded in Gulf | 2,000 vessels |

| Mariners affected | 20,000 |

| Monthly oil price increase | Largest in history |

III. The Global Economic Cascades

Europe’s Second Energy Crisis

Europe entered the crisis in a state of acute vulnerability. A harsh 2025–2026 winter had depleted gas storage to 30 per cent of capacity—historic lows for early spring. The Dutch Title Transfer Facility benchmark, Europe’s primary gas pricing mechanism, nearly doubled to over €60 per megawatt-hour by mid-March. The European Central Bank, which had anticipated interest rate cuts to stimulate sluggish growth, instead postponed monetary easing, raised inflation forecasts, and slashed GDP projections. Germany, the United Kingdom, and Italy faced the highest recession risk since the 2008 financial crisis.

The industrial impact was severe. German chemical and steel manufacturers, already battered by the 2022 energy shock, imposed 30 per cent fuel surcharges on customers. BASF, the world’s largest chemical producer, warned of “permanent deindustrialisation” in energy-intensive sectors if prices remained elevated beyond the second quarter. As ECB President Christine Lagarde told the European Parliament, “We are not facing a supply disruption. We are facing a supply dislocation of a magnitude unseen in fifty years.”

Asia’s Vulnerability Exposed

Asia’s dependency on Hormuz is structural and overwhelming. Sixty per cent of the continent’s petroleum originates in the Middle East; China, India, Japan, and South Korea alone account for 75 per cent of Gulf oil exports and 59 per cent of LNG shipments. The Asian Development Bank projected that developing Asia’s growth would be cut by up to 1.3 percentage points—sufficient to push several economies into technical recession.

China’s position is particularly fraught. Beijing relies on Hormuz for approximately 40 per cent of its oil imports, yet simultaneously supports Iran strategically through intelligence sharing, satellite cooperation, and dual-use technology transfers. This creates a tension between economic necessity and geopolitical alignment that Chinese strategists have long feared. As Professor Shi Yinhong of Renmin University noted, “China cannot afford a closed Hormuz, yet it cannot afford an Iranian collapse. The blockade forces a choice Beijing hoped to defer indefinitely.”

The Global South’s Pain

The crisis has hit the developing world hardest. Gulf states, paradoxically, rely on the strait for 80 per cent of their caloric intake—food imports transited through the very chokepoint they helped close. By mid-March, 70 per cent of regional food imports were disrupted; consumer prices for staples spiked 40 to 120 per cent. The Philippines declared a state of emergency; Zimbabwe, Pakistan, Bangladesh, Nigeria, and Vietnam faced severe fuel shortages that threatened power generation and agricultural planting seasons.

The fertiliser crisis compounds the damage. Brazil, which accounts for 60 per cent of global soybean exports, depends on Hormuz-transited potash and phosphate. Chilean copper mining, critical for global electrification, has been hit by sulphuric acid shortages. The United Nations Development Programme estimates that Arab nations alone face GDP losses of $120 to $194 billion—figures that do not capture the humanitarian catastrophe unfolding in import-dependent African and South Asian states.

| Regional Economic Impact Assessment | ||

|---|---|---|

| Region | Primary Impact | Severity |

| Europe | Gas price doubling, industrial surcharges | Severe |

| East Asia | LNG rationing, growth cut 1.3% | Severe |

| South Asia | Fuel shortages, agricultural disruption | Critical |

| Gulf States | Food import collapse, price spikes 40–120% | Critical |

| Latin America | Fertiliser shortage, mining disruption | Moderate–Severe |

| Sub-Saharan Africa | Emergency fuel deficits, humanitarian crisis | Critical |

The American Paradox

The United States, shielded by domestic shale production and Canadian imports, is less directly exposed than import-dependent economies. Yet American consumers have not escaped unscathed: gasoline prices rose to $4 per gallon by late March, the highest since 2023. Trump, characteristically, dismissed the pain. “If they rise, they rise,” he told reporters. “We have a war to win.”

The fiscal cost, however, is staggering. The Congressional Budget Office estimates war expenditures exceeding $200 billion, with arms production quadrupled to sustain interceptor supplies depleted by Iranian missile barrages. The paradox is stark: America is paying unprecedented costs to prosecute a blockade whose primary victims are its own allies and the global economy it purports to lead.

IV. The Great Power Dimension: China’s Shadow War

Intelligence and Technology Support

Whilst Beijing publicly calls for “restraint” and “freedom of navigation,” its covert support for Tehran has transformed the military balance. Leaked Iranian documents reveal that the IRGC secretly acquired a Chinese reconnaissance satellite—operated by Earth Eye Co., a firm with documented links to the People’s Liberation Army—in late 2024. The satellite has been used to target U.S. bases and naval assets with precision previously beyond Iranian capability.

More significantly, Iran has integrated China’s BeiDou satellite navigation system into its ballistic missile guidance architecture, reducing dependence on GPS and rendering Western jamming techniques ineffective. U.S. intelligence has detected Chinese weighing of transfers of X-band radar systems and man-portable air-defence systems (MANPADs) to Iran through third countries, including North Korea and Syria.

The dual-use trade is equally troubling. In February 2026, U.S. naval forces seized the Iranian vessel MV Touska returning from China with cargo described as “dual-use industrial equipment” but suspected to contain precision machining tools for missile production. Chinese semiconductor giant SMIC stands accused of providing chipmaking tools to Iran’s military programme—allegations Beijing denies but which align with documented patterns of technology diversion.

The Strategic Calculus

China’s support for Iran is not sentimental solidarity but cold strategic calculation. The 2026 war provides Beijing with an unparalleled live testing ground for evaluating Western military capabilities—missile defence architectures, stealth aircraft performance, electronic warfare effectiveness—without risking a single PLA soldier. As one Chinese military analyst wrote in a restricted-circulation journal, “Let the Americans and Israelis reveal their capabilities against Iranian proxies. We shall take notes.“

Simultaneously, the Hormuz closure exposes the fragility of China’s maritime-dependent Belt and Road Initiative, accelerating interest in overland alternatives. The China-Pakistan Economic Corridor, the China-Central Asia-West Asia Economic Corridor, and the nascent China-Iran rail link have all received emergency funding boosts since March. Beijing is learning, painfully, that maritime dominance without chokepoint control is a hollow asset.

The U.S.-China Energy War

The crisis has crystallised a competition between two competing visions of Eurasian connectivity. The India-Middle East-Europe Economic Corridor (IMEC), unveiled at the 2023 G20 summit and championed by Washington, is designed to bypass Hormuz entirely through rail, pipeline, and port infrastructure linking India to Europe via the UAE, Saudi Arabia, Jordan, and Israel. The Belt and Road Initiative, by contrast, remains heavily maritime-dependent, with 60 per cent of Chinese energy imports transiting the strait.

The UAE’s dramatic 29 April announcement of its OPEC exit—freeing 4.85 million barrels per day of production capacity from cartel quotas—signals Abu Dhabi’s strategic alignment with the Western-led IMEC framework over Chinese economic partnerships. As Karen Young of the Middle East Institute observed, “The Emiratis have made their bet. They see the future in overland corridors and Western security guarantees, not in maritime dependency and Chinese ambiguity.”

| China-Iran Military Cooperation: Documented Activities | |

|---|---|

| Capability | Details |

| Reconnaissance satellite | Earth Eye Co. satellite acquired late 2024; targeting U.S. bases |

| Navigation systems | BeiDou integration for missile guidance; GPS independence |

| Radar technology | X-band radar systems under consideration for transfer |

| Air defence | MANPADs via third-country routing |

| Dual-use trade | MV Touska seizure; SMIC chipmaking tools allegations |

| Strategic benefit | Live evaluation of Western military systems |

V. The Alliance Fracture: NATO and the End of Omni-Alignment

NATO’s Iran Rupture

Trump’s request for NATO allies to support the Hormuz blockade has exposed the alliance’s deepest fissures since the 2003 Iraq War. The United Kingdom offered limited naval support—principally mine-countermeasures vessels and intelligence assets—but France and Germany restricted their contributions to logistical assistance. Spain refused entirely, with Prime Minister Pedro Sánchez stating that “NATO’s purpose is collective defence, not offensive blockades in distant waters.“

The alliance officially sat out the U.S. operation, issuing no collective statement of support. This abstention is not merely diplomatic caution; it reflects a fundamental divergence in threat perception. European capitals view Iran through the lens of nuclear non-proliferation and regional stability; Washington views it through the prism of great-power competition and Israeli security. As Dr. Garret Martin of American University noted, “NATO cohesion is under severe strain. The Iran issue has become a proxy for broader doubts about American reliability and strategic judgment.“

European leaders are now quietly contemplating “Plan B” alternatives should Trump withdraw from NATO entirely—a scenario no longer considered implausible in Brussels or Berlin. The French proposal for European strategic autonomy, long dismissed as Gaullist nostalgia, has gained urgent credibility.

The Gulf’s Hedging Strategy Collapses

For two decades, Gulf monarchies practised “omni-alignment”: securing U.S. security guarantees, cultivating Chinese economic partnerships, and maintaining Iranian détente through back channels. The 2026 war has rendered this strategy impossible. The UAE’s OPEC exit on 29 April—announced without prior consultation with Riyadh—marks the most dramatic manifestation of this collapse.

The Saudi-Emirati divergence is instructive. Saudi Arabia, under Crown Prince Mohammed bin Salman, has joined Pakistan, Egypt, and Turkey in seeking a diplomatic solution, hosting indirect talks and offering humanitarian corridors. The UAE, by contrast, demands harder guarantees against future Iranian threats and has accelerated its military modernisation programme, signing $19 billion in new defence contracts with American and European suppliers in April alone.

The IMEC Imperative

The India-Middle East-Europe Economic Corridor is no longer diplomatic window-dressing but a strategic necessity. Saudi Arabia is reviving its East-West pipeline—a 1,200-kilometre conduit with 7 million barrels per day of capacity to the Red Sea port of Yanbu—as an emergency bypass for Hormuz. India has fast-tracked port upgrades at Mundra and Kandla to handle redirected Gulf crude. The corridor’s transformation from G20 talking point to survival mechanism represents one of the most significant geopolitical pivots of the decade.

| Alliance Responses to Hormuz Blockade | ||

|---|---|---|

| Actor | Position | Action |

| United Kingdom | Conditional support | Mine-countermeasures, intelligence assets |

| France | Restricted support | Logistical assistance only |

| Germany | Restricted support | Logistical assistance only |

| Spain | Opposition | Refused participation |

| NATO (collective) | Abstention | No official statement of support |

| Saudi Arabia | Diplomatic solution | Hosted talks, humanitarian corridors |

| UAE | Hardline alignment | OPEC exit, $19bn defence contracts |

| Pakistan | Mediation | Hosted U.S.-Iran talks 7–8 April |

| China | Strategic ambiguity | Vetoed UN resolution, covert support for Iran |

| Russia | Pro-Iran alignment | Vetoed UN resolution, military advisors |

VI. International Law and the New Chokepoint Economy

The Legal Vacuum

The dual blockade has created a legal vacuum that threatens the foundations of maritime commerce. Iran’s mining and closure violate UNCLOS Article 44; the U.S. counter-blockade, whilst framed as self-defence and counter-proliferation, creates legal ambiguity that weakens the very norms Washington claims to uphold.

The United Nations Security Council has been paralysed. On 7 April, Russia and China vetoed a Bahrain-drafted resolution demanding Iranian compliance with transit passage obligations. In response, 37 countries—including the UK, France, Japan, Australia, and Canada—signed a joint statement affirming the right of safe passage and threatening “collective measures” to enforce it. This coalition-of-the-willing approach, reminiscent of the 2003 Iraq precedent, further erodes the UN’s authority.

The toll controversy illustrates the legal chaos. Iran suggested charging transit fees for strait passage—a proposal the UK rejected as violating UNCLOS. Trump reportedly floated a “joint venture” to share proceeds from Hormuz transit fees with regional partners—a concept legally untenable under international law but revealing of the transactional mindset shaping American policy.

The Insurance Crisis

Without security guarantees, commercial insurance for Hormuz transit has become prohibitively expensive or entirely unavailable. The Joint War Committee has declared the strait and adjacent waters a “Listed Area,” triggering automatic premium increases of 500 to 1,000 per cent. Many underwriters have simply withdrawn coverage, forcing national governments to assume risk or shippers to self-insure—neither sustainable at scale.

Alternative routing via the Cape of Good Hope adds 7,000 nautical miles and three weeks to voyages from the Gulf to Europe, whilst the Bab-el-Mandeb strait—already threatened by Houthi entry into the war on 28 March—offers no reliable alternative. The world’s maritime insurance architecture, built on the assumption of chokepoint stability, is facing an existential stress test.

VII. Conclusion: The Post-Hormuz World

Even if the strait reopens tomorrow—and the ceasefire brokered in Islamabad on 7–8 April remains fragile, with direct U.S.-Iran talks on 11–12 April yielding only tentative progress—the war has permanently altered global energy psychology. No chokepoint will ever be trusted again.

Three structural consequences are already discernible.

First, decoupling from chokepoints. The crisis has transformed IMEC from diplomatic aspiration to strategic imperative. Overland corridors, pipeline networks, and alternative maritime routes will receive unprecedented investment. The geography of global energy is being redrawn not by market forces but by strategic vulnerability.

Second, OPEC’s decline. The UAE’s exit marks the beginning of the cartel’s fragmentation. Sovereign energy policy is trumping collective management as producer states prioritise security over price stability. Saudi Arabia may follow; the era of coordinated production management is ending.

Third, alliance reconfiguration. The end of “omni-alignment” forces binary choices between American and Chinese spheres. Neutrality is no longer sustainable when energy security is at stake. The Gulf states, Europe, and even Southeast Asia are being compelled to choose sides—a process that will reshape international relations for a generation.

Trump’s Hormuz gamble has achieved its immediate military objective of pressuring Iran. Tehran’s economy is suffocating, its currency collapsing, and its population restive. Yet the cost has been the acceleration of the very multipolar fragmentation the United States sought to prevent. The blockade is a tactic; the transformation it has unleashed is strategic, structural, and permanent. The post-Hormuz world is being born in fire—and its final shape will define the twenty-first century.

As the ancient Greek historian Thucydides might have observed of our own age: “In the contest for power, the strong do what they can, and the weak suffer what they must.” In the Hormuz gamble, it is not yet clear which power is which.